Compared to many western nations, China handled the early stages of the COVID-19 pandemic relatively effectively. The country locked down quickly to limit the spread of infection and made testing materials widely available to track the virus’ transmission. As a result, the early waves of COVID were addressed rapidly in China whereas, in western nations, arguments over how far PPE and vaccination mandates could go meant infections were allowed to spiral out of control.

Now, more than two years following the outbreak, many countries have accepted that COVID-19 is now endemic and have mostly removed lockdown and PPE mandates in an effort to allow normal lifestyles to resume. China, however, has stood as something of an outlier, retaining its strict ‘zero-COVID’ policy and enforcing severe lockdowns on major population centers in an effort to stamp out the virus. Naturally, this has caused friction across many industries, with automotive production and sales being significantly disrupted.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

What May’s sales figures tell us

Finally, after a couple of months of dramatically reduced output and sales across many major Chinese cities, May’s numbers indicate a recovery is taking hold in the country.

It’s important to note that the rebound in sales numbers is being directly driven by a recovery in Chinese vehicle production which, throughout March and April, had been either halted or significantly curtailed by COVID lockdown orders. However, production picked up pace towards the end of April and into May, driven by what is euphemistically referred to as ‘closed loop’ production networks – i.e. factory workers essentially being made to live and sleep at their workplaces.

The impact of a stronger May has pushed China’s seasonally adjusted annualized selling rate (SAAR) to 23.7 million units – a 66.4% increase on the SAAR figure for April. Despite the good news provided by May’s vehicle sales figures, China’s overall vehicle sales are down by 8% for the year to date, highlighting the bruising the country took from its strict lockdown orders.

The recovery in production and sales was predominantly driven by stronger performance in the passenger car sector, whereas sales of light commercial vehicles such as vans performed much worse. The overall year-on-year decline seen for passenger cars in May was just 1.3%, compared with 40% for LCVs, which dragged the overall picture down.

Echoing recent Chinese sales results, new energy vehicles (NEVs, including BEVs and PHEVs) retained their strong rate of growth, despite the wider disruption affecting the market. NEV sales for the year-to-date are up by 116% to more than 440,000 units.

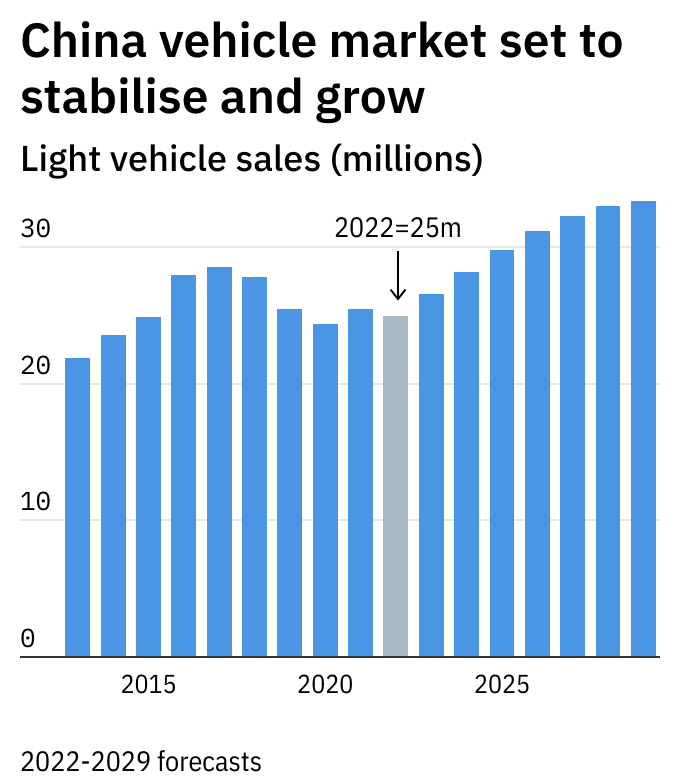

Looking further out, we’re forecasting that the recovery in Chinese sales and production will accelerate throughout 2022. By the end of the year, we expect the SAAR for light vehicles to crest 27 million units – a level that has not been seen since 2020, and approaching pre-pandemic levels.

A factor that is likely to strengthen the Chinese vehicle sales landscape is the recently announced reduced tax incentive for which more than 70% of the Chinese new vehicle market will be eligible – not just the normally favored NEVs. China’s new vehicle buyers have proven to be highly sensitive to such incentives in the past and, were it not for some likely residual problems in the supply chain, we might expect genuinely explosive growth in the second half of the year. As it stands, strong recovery is what is anticipated.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center