With the pandemic closing facilities and severely disrupting supply chains, a global chip shortage endangering manufacturing rates, and changing consumer habits and government legislation producing a pivot towards EV production, the automotive industry has had multiple challenges to navigate. Yet despite all this, the market is performing better than expected and is recovering strongly.

“I’m very optimistic on the marketplace,” says Jeff Schuster, vice-president of automotive research at GlobalData. “This is an exciting time for auto, and I think an exciting time to watch this transition play out. Those that do it well will certainly be winners.”

The resilience of the automotive market

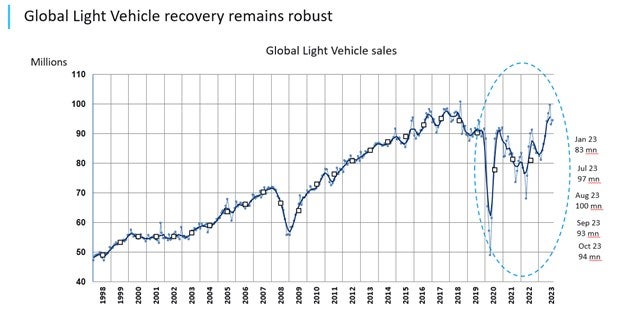

Looking at the global automotive market, light vehicle (LV) sales have once again rebounded to exceed slightly pre-pandemic levels, although they have yet to match the heights of 2018 sales. Recovery has been somewhat slower compared to the financial crisis of 2008. However, there was a much faster fall and rebound between 2020 and 2021 than over 2008-2009 – but also a far sharper fall beforehand.

Nevertheless, the global market continues to outperform expectations, with the global GDP growing by 2.5% in November 2023. Notably, China continues to outperform the rest of the world in this market. China’s GDP was up by 5.1% in November 2023, compared with 2.1% in the US and 0.5% in the Eurozone, with month-on-month growth forecast to continue around the 5% mark throughout 2024.

China also looks to have the largest appetite for EVs, with battery electric vehicles (BEVs) taking a 22.6% share of automotive sales in that region in 2023, compared with 7.4% in the US and 14.3% in Europe.

However, the EV market in these two significant regions is only set to grow more rapidly. BEV sales were up by 63% in the US as of September 2023 and 49% in Europe, whereas sales in China increased by 32% across the same period.

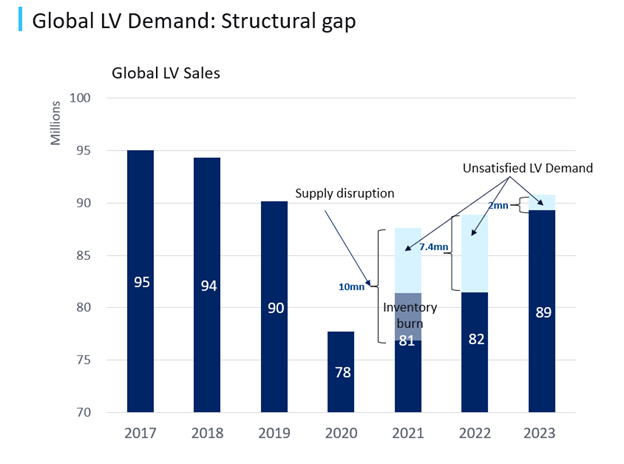

As for the LV market, there remains a structural gap between supply and demand on account of supply chain disruption. Without the LV inventory cushion, 2021 global sales would not have exceeded those of 2020. In 2022, GlobalData research estimates that underlying full-year LV demand was 7.4 million above sales.

Analyzing market data for the US automotive

US sales remained robust in the last 12 months, with LV sales up 13% year-on-year as of November 2023. Daily selling rates peaked in May and, whilst forecast to level off moving forward, have remained comfortably above 2022 levels.

Growth has been enabled by a decent economy, stable pricing, and the return of incentives. The UAW strike somewhat inhibited the market’s recovery, but a reduction in overall disruption and inventory levels being at their highest since March 2021 meant production grew by 9% across 2023, with further growth predicted into 2024.

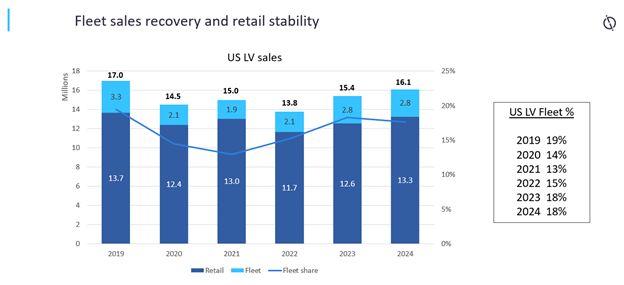

Alongside the recovery of US production, a key factor in driving change has been the recovery of fleet sales and retail stability. Both fleet and retail have outperformed expectations since the beginning of the year, but GlobalData predicts that the boost from fleet is fading and that sales will likely match 2023 figures in 2024. Future market growth will be more dependent on retail.

Moreover, strong premium sales have contributed to the stabilization of the US automotive market, contributing to 17.4% of sales in 2023 – a significant rise compared to pre-pandemic annual market shares in 2018-2019 of around 13%. GlobalData predicts that the market share of premium vehicles will continue to rise going forward.

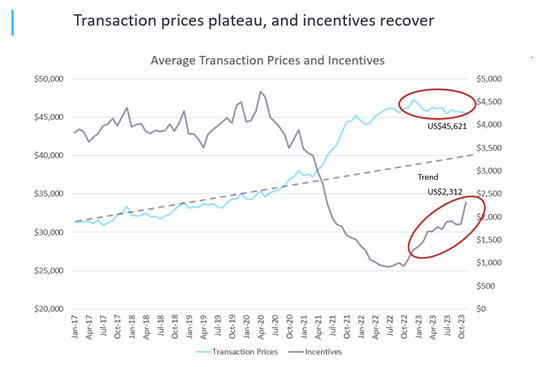

Despite these positive developments, challenges remain for the US market. Whilst inflation was down to 4.2% across 2023 from 8% the previous year, transaction prices remain 33% higher on average compared with pre-pandemic levels. This has likely priced many potential buyers out of the market, alongside the cratering of incentives in July 2022. Incentives may have since more than doubled, but they remain around 55% below what they were in early 2020 despite rises driven by Black Friday.

Over the past few years, dealerships have flourished from selling fewer cars at much higher margins, with every vehicle coming into the dealership sold. Profits have been maintained, but at what cost?

“I think the main issue in the US is going to be around pricing and how much the new car market can grow going forward, and whether it needs to,” says Schuster. “I think what the pandemic taught the industry is, and this is used, certainly in other parts of the world, Japan and Korea come to mind, in particular, is not to over build.”

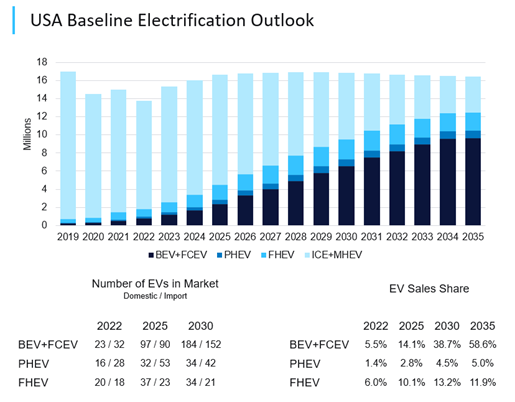

Issues also remain in the US for EVs, not least in terms of infrastructure, with charging stations unable to meet the demand from the number of plug-in cars. In the US, there are around 487 cars per DC fast-charging station, illustrating how infrastructure to support EVs must be scaled up to meet public demand.

This is a demand that is only forecast to grow. EVs may have less than a 10% share of the US automotive market right now, but this is projected to soar to a more than 70% share by 2035, according to GlobalData modeling. This is positive news for the EV market, but growth must be supported by sufficient charging infrastructure moving forward.

Opportunities for automotive dealerships

In a changing market with prices remaining high, it is more important than ever that dealerships provide high-quality customer service to support sales and brand awareness.

“There are quite a range of customer relationship management (CRM), platforms and tools that are out there, and they’re becoming increasingly sophisticated,” says David Leggett, Editor of Just Auto. “I think it’s about really communicating with the customers and understanding what their needs are. But a big part also is the willingness to do it, to actually invest in the software and the skills needed to really max out on the usefulness of the tools that are increasingly available.

“With advanced technologies, such as AI, some of these tools are becoming vital to be a successful dealership and really grow the business.”

The market model for OEMs is changing, with online retail potentially offering the chance to cut out the dealerships in the middle and sell directly to consumers. Yet despite these potential risks, Leggett sees this customer service element as the key to success for dealers going forward.

“The dealer is actually in quite a strong position in terms of the relationship with the customer,” he explains. “That’s the thing that the dealer really has to focus on. It’s how you develop that relationship, how you really engage with the customer, and keep the customer happy, particularly in these very uncertain and potentially volatile times.”

When it comes to customer satisfaction, there are new solutions to put dealerships in the best position going forward. Uber for Business facilitates a seamless customer experience by offering rides home, or to work, for customers awaiting vehicle repairs or a new car. Rather than relying on a loaner car or shuttle service, dealers can request rides using Uber Central to transport customers or even to pick up and return parts, including batteries.

With the transition to EVs showing no signs of stopping, dealerships have the potential to maximize the tools at their disposal to reassure customers in the purchase of new and unfamiliar technology. “I think the dealers are in a really strong position to bid to be an active part in that transition,” states Leggett.

To gain more data-driven insights into how the US automotive dealers are responding to new demands, follow the link to access the exclusive GlobalData webinar, titled ‘Shifting gears: How US automotive dealers are evolving their offering to reflect changing customer needs’.