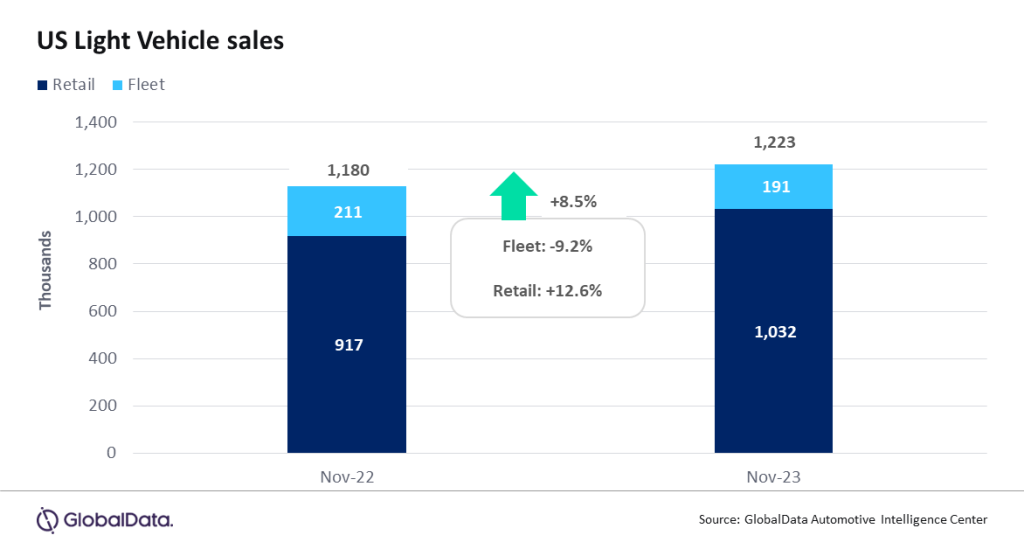

According to preliminary estimates, US Light Vehicle (LV) sales grew by 8.5% year-on-year (YoY) in November, to 1.22 million units. The YoY growth was helped by weak sales a year ago. While the results were a little lower than expected, the selling rate is at a similar pace to recent months.

However, with inventory improving, it seems that customers are having to be enticed with higher incentives than has been the case since the onset of the chip shortage.

US LV sales totaled 1.22 million units in November, according to GlobalData. The annualized selling rate was 15.4 million units/year in November, down from 15.6 million units/year in October. The daily selling rate was estimated at 48.9k units/day in November, compared to 48.2k units/day in October. Despite the uptick in the daily selling rate, it appears that November sales were slightly disappointing, with Thanksgiving and Black Friday sales not delivering quite as robust an acceleration as hoped. According to initial estimates, retail sales totaled around 1.03 million units, while fleet sales accounted for approximately 191k units, representing around 15.6% of total sales.

David Oakley, Manager, Americas Sales Forecasts, GlobalData, said: “With the UAW strikes over, the industry could focus on more typical matters of LV demand and the extent to which Thanksgiving sales would spur the market, against the backdrop of many households feeling squeezed and interest rates remaining high. In the end, sales grew by 8.5% YoY, but there was a feeling that results could have been better. While consumers still appear willing to spend, many are remaining more cost-conscious, and this is forcing the industry to begin to offer higher incentives, even if discounting remains well below historical averages for now. In addition, several models that were directly impacted by the UAW strikes were still suffering from low inventory in November, and that appeared to restrict their sales. Had these models delivered more typical volumes, the overall market’s performance would have looked more robust”.

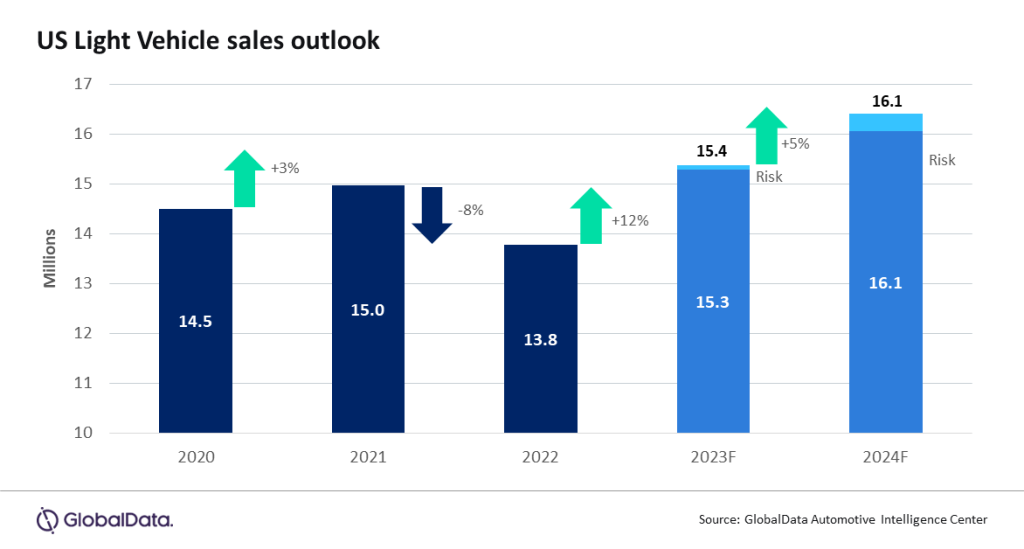

The year-to-date (YTD) sales market continues to deliver at or above expectations and 2023 remains on track to reach 15.4 million units, up 12% from 2022. Given the stability in demand and supply constraints being reduced, we have increased the forecast for 2024 to 16.1 million units from 16.0 million units.

The YTD daily selling rate is at 50.2k, up from 44.6k last year, though October and November were both under the YTD average. Inventory levels remain sufficient to support demand at an industry level. Days’ supply is expected to be at 45 days, which is flat from last month. Inventory volume is projected at 2.25 million units, up from 2.16 million units in October.

At an OEM level, Toyota Group outsold General Motors for the second consecutive month, but this time by a very tight margin of just 178 units. Both OEMs’ market shares rounded to 16.2%, which was down by 0.1 pp month-on-month (MoM) in Toyota’s case, but up by 0.6 pp MoM for General Motors, as the latter recovered from the UAW strikes. Ford Group was the third-largest OEM on 140k units, although at 11.4%, its market share was the lowest since August 2021. At a brand level, Toyota easily led the rankings with 167k units, some 33k ahead of Ford, which only beat Chevrolet by 3k units. The Toyota RAV4 was the bestselling model for a second straight month with 42.8k units, finishing 10k ahead of the Ford F-150. The RAV4 has been boosted by an unusually high level of imports in recent months, but this is understood to be a temporary situation. Compact Non-Premium SUV was once again the number one segment, setting a record-high market share for the third consecutive month, at 21.1%. Midsize Non-Premium SUV was a distant second on 15.5%, followed by Large Pickup on 13.6%.

Jeff Schuster, Vice President Research and Analysis, Automotive, said: “While there isn’t much outlook ahead for 2023, the stability in the market is setting up next year fairly well, despite some headwinds with the overall economy and general pricing trends. Consumers should have more choices next year, which could also be a pivotal year in measuring the speed of the transition to electrification. Several brands have revised the near-term outlook, but investments have been made, so 2024 is shaping up as an important indicator to the health of the overall industry, and, more specifically, to the traditional OEMs.”

Global outlook: October was another strong month for global LV sales as the selling rate hit 94 million units and volume increased by 10.7% from October 2022. This represented the fifth consecutive month above 90 million units. Many key markets saw double-digit growth, but October 2022 was a weak base for comparison. November is expected to have ended above the 90-million-unit level again, setting up a strong close to the year. With less than one month to go in 2023, the outlook for global LV sales has been revised upward yet again on the strength of China’s wholesale market. The 2023 forecast now stands at 89.2 million units, up 600k units from a month ago and equating to a 10.0% increase compared to 2022. Note – GlobalData will be moving to reporting and forecasting domestic sales in China, thus lowering the market by 3.7 million units. For 2023, our current forecast of 92.3 million units is holding.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center