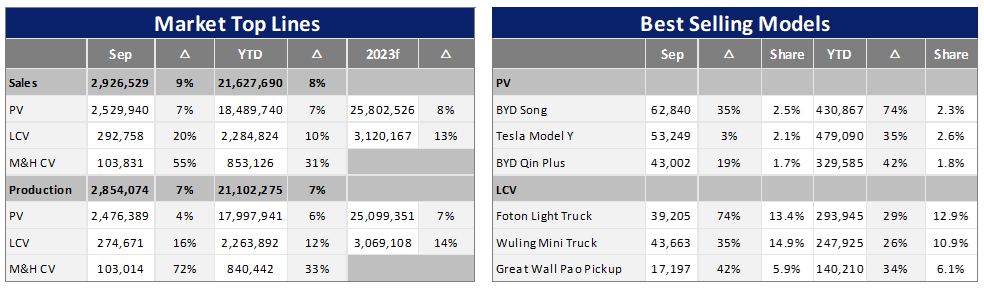

The Chinese market maintained a robust pace in September 2023 with Light Vehicle (LV) wholesales increasing by 8% year-on-year (YoY) to 2.8 million units. At a component level, Passenger Vehicle (PV) sales (i.e., wholesales) increased by 7% YoY to 2.5 million units in the month. At the same time, the Light Commercial Vehicle (LCV) sector grew rapidly by 20% YoY, with sales of 0.3 million units. On a month-on-month (MoM) basis, PV sales increased by 9%, while LCV demand was boosted by 20% in September.

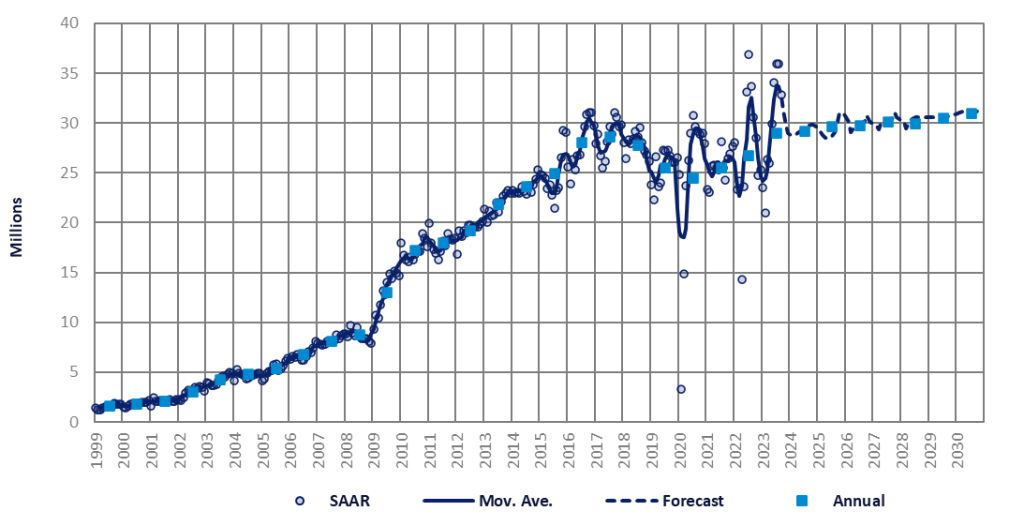

Since the beginning of this year, cumulative LV wholesales have totalled 20.8 million units which is an increase of 7% over the same period last year. The strong market performance in September led to a selling rate for the month of 32.9 million units/year. While it was 9% lower than the unusually strong August, this is still a very high level. The average year-to-date (YTD) selling rate is 29.5 million units/year, far exceeding last year’s total LV sales of 26.7 million units.

In terms of production, total LV build in September was 2.8 million units, a YoY increase of 5%. At a vehicle type level, PV production (accounting for 90% of total LV production) in September was 2.5 million units, a YoY increase of 4%. Cumulative PV production was 20.3 million units, a YoY increase of 7%. CV production in September was 0.3 million units, which equates to rapid YoY growth of 16%. Year to date (as of September), LV cumulative production has reached 2.3 million units, a YoY increase of 12%.

As has been the case in recent months, a boom in exports, especially of new energy vehicles (NEVs), drove wholesale sales in September. In the month, PV exports increased by 54% YoY, while the cumulative YoY increase was 70%. According to data from the China Passenger Car Association (CPCA), the main destinations for China’s PV exports in the first seven months of 2023 were Russia (accounting for 16.7% of total PV exports), Mexico (8%) and Belgium (5.4%). Affected by the economic sanctions imposed by Western countries on Russia, China’s exports to that country have increased significantly this year.

In contrast, PV sales in the domestic market only increased by 1.5% YoY in September, and the cumulative YoY growth in the first nine months of 2023 was 0.2%. However, this is still a good result, because the demand rebounded a year ago due to the epidemic lockdown, resulting in a very high sales growth rate. In August 2023, Tesla launched a new round of price cuts, triggering a wave of large-scale cuts by other major automakers. And according to current market activity, this trend of price reduction promotions will continue until next year.

An increasing number of affordable models with advanced features are attracting consumer interest. Of course, this wave of price cuts will also further reduce OEM vehicle profits. Unless more cars are sold, their overall profitability will be significantly reduced. It is foreseeable that in the next few years, OEMs that cannot capture a substantial piece of the market may leave the game.

Following the market’s weak performance in early 2023, in recent months the Chinese government has introduced a series of macro measures to stabilise economic growth and promote automobile consumption. Strong national finance measures will firmly support the development of the automobile market. At present, market confidence has been enhanced, production demand has simultaneously recovered, and OEMs are constantly launching new products, all of which will help to release further market demand. Hence, we believe that in the next few years, China’s automobile industry will achieve steady growth driven largely by the growth of exports and domestic NEV demand.

Therefore, we expect sales to remain strong in the coming years. This month we have again increased our full-year 2023 forecast, this time by 300,000 units, bringing the full-year forecast to 28.9 million units, a year-on-year increase of 8%. However, it should be noted that near-term downside risks exist, mainly from the liquidity crisis in the real estate sector (said to directly and indirectly account for 25% of GDP), declining exports, and high youth unemployment.

On the other hand, we have lowered our sales forecast for 2028 by 534,000 units, 2029 by 538,000 units, and 2030 by 198,000 units per year, as the step decline of the temporary purchase tax reduction for NEVs in 2025 and 2027 will directly affect overall sales. The faster-than-expected ageing of the population is another factor in lowering the long-term forecast. The UN forecasts that by 2035, people aged 65 and over will account for 21% of China’s population, more than a percentage point higher than previous forecasts.

At present, the China automobile market is in a stage of rapid development. With the continuous progress of science and technology and the improvement of environmental protection requirements, the automobile industry is facing unprecedented challenges and opportunities. The positioning of the Chinese market for automobiles is changing from mechanical systems to durable consumer electronics, which may make the use cycle of automobiles greatly shorter, and given the huge population base, there is room for further improvement in China’s car ownership levels in the future.