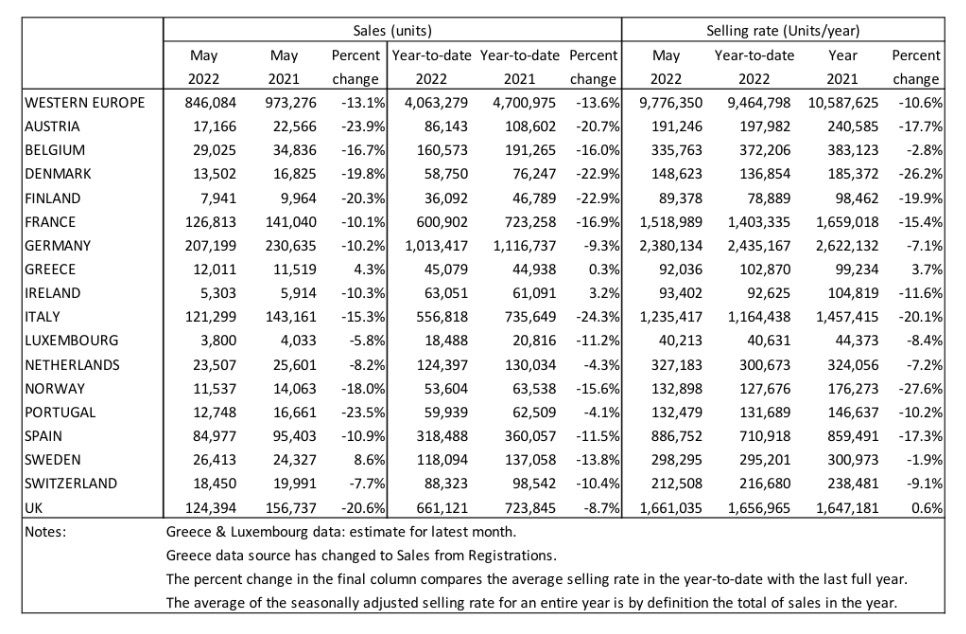

Although it was down 13.1% versus last year, the West European car market annualised selling rate (SAAR) increased to 9.8 mn units/year in May, from 8.8 mn units/year in April, according to GlobalData unit LMC Automotive.

While the demand environment this year has become increasingly challenging, as consumer confidence has made a step-change down since the start of the war in Ukraine, it remains the supply side of the automotive industry that holds back better registration statistics.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

The German car market selling rate improved to 2.4 mn units/year in May, from 2.0 mn units/year previously, though remains low by historical standards. In the UK, the selling rate remained broadly flat on the month before at 1.7 mn units/year. For France, the selling rate increased to 1.5 mn units/year, from 1.2 mn units in April. While in Spain, the selling rate rose to a 2022 high of 887k units/year. Finally, the Italian PV selling rate improved modestly on the month before to 1.2 mn units/year.

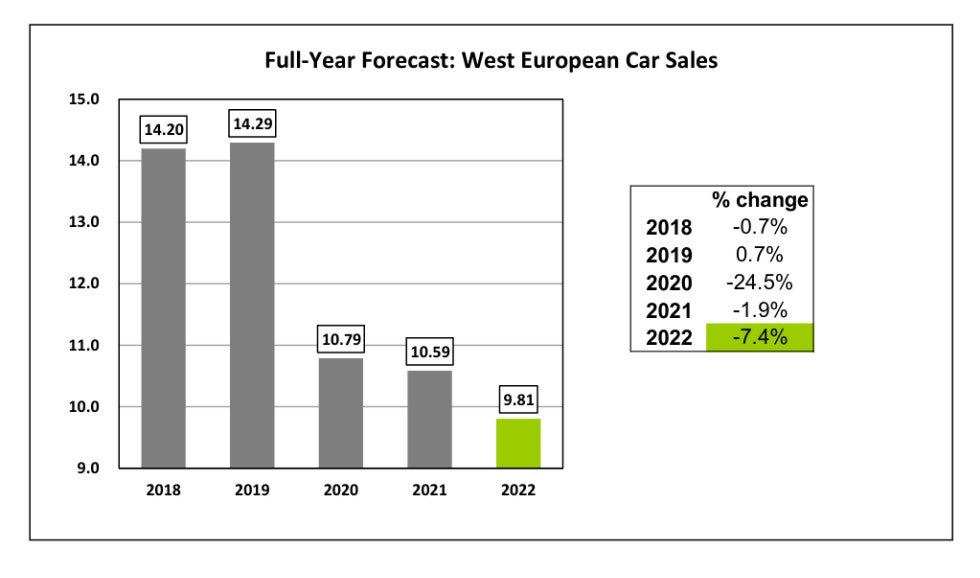

LMC forecasts the 2022 West European car market down against both 2020 and 2021, and at around two-thirds of the levels seen in 2019, due to the baseline assumption that supply chain issues will constrain results through this year and into 2023. LMC says risks still lie tilted to downside, with the most immediate threat to the forecast posed by a longer-than-expected conflict in Ukraine or worsened supply chain disruption because of China’s COVID-19 policy. Moreover, the demand side situation is becoming increasingly gloomy, highlighted by the fact that consumer confidence in Europe is currently lower than anything seen at the start of the pandemic.