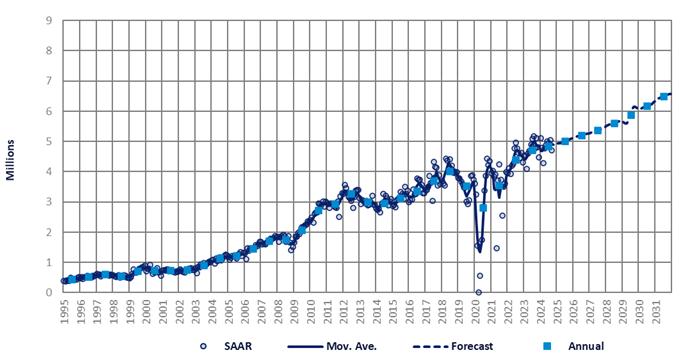

The Indian market has lost some momentum, with the September selling rate falling by 7% from August to 4.7 million units. Despite this slowdown, the market continued to maintain a strong pace.

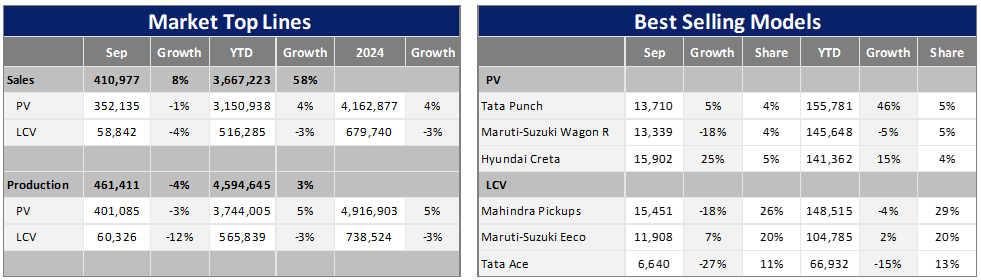

In September, a total of 411k Light Vehicles (LVs) were sold in the country. This represented a 2% month-on-month (MoM) increase, but a 2% year-on-year (YoY) decrease. Passenger Vehicle (PV) wholesales stood at 352k units (+1% MoM, -1% YoY), while sales of Light Commercial Vehicles (LCVs) with a gross vehicle weight of up to 6T amounted to 59k units (+10% MoM, -4% YoY).

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

PV wholesales have declined YoY for the third consecutive month, impacted by sluggish demand and stock corrections from automakers to reduce high inventory at dealerships. Similarly, LCV sales were affected by the extended monsoon period, tight credit availability and higher vehicle prices, as well as low government spending. Consequently, LCV volumes have decreased YoY for five successive months.

According to data from the Federation of Automobile Dealers Associations (FADA), retail sales of PVs and LCVs in September slumped to 317k units, from 352k units in August and 365k units in July.

Retail sales did not improve during the auspicious festivals of Ganesh Chaturthi and Onam, while demand was also negatively impacted by the Pitru Paksha (or Shraddh) period from September 17 to October 2, 2024, during which Hindus defer celebratory purchases. In addition, showroom traffic was further hindered by heavy rainfalls.

As a result, PV inventory hit a new high of 80-85 days, equivalent to 790k vehicles, at the end of September, as reported by FADA. This marks an increase from 70-75 days, equivalent to 780k vehicles, at the end of August.

Overall, LV sales from January to September improved by 3% YoY to 3.7 million units. This figure comprised 3.2 million PVs (+4% YoY) and 516k LCVs (-3% YoY).

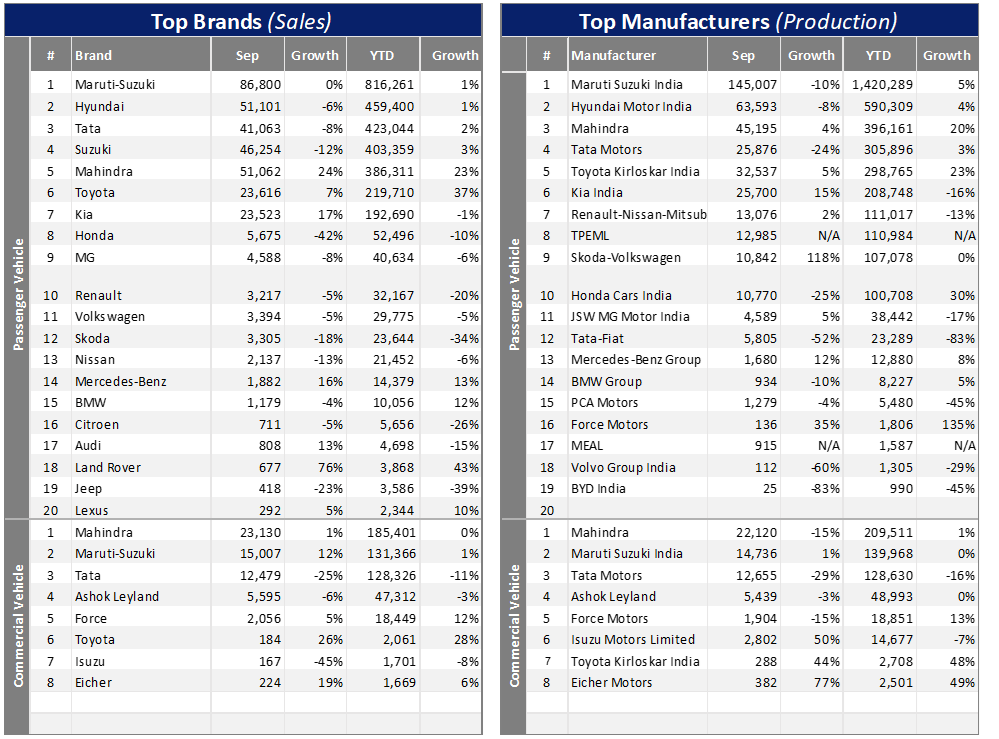

Preliminary data for October from the top five OEMs shows that market leader Suzuki Group’s PV wholesales grew by 11% MoM. Meanwhile, Hyundai improved its volumes by 9% from the previous month, and Tata Motors’ PV sales surged by 17% MoM. In addition, Mahindra, benefiting from the consistent demand for SUVs, raised its wholesales in October by 7% compared to September. Finally, Toyota saw its volumes (mostly PVs) expand by 19% MoM.

The robust growth was largely influenced by the popular festivals of Navratri, Dussehra, Dhanteras, and Diwali, which usually span over two months but occurred in October this year. As such, there is some indication that PV retail sales increased during the month as a result of heightened demand during these festivals.

We remain cautiously optimistic in terms of the sales outlook. Although September sales were weaker than expected, wholesales were still high. The expected launch of several new models and generations will likely continue to attract consumers’ interest, especially in the SUV segment.

Plus, the FY2024/2025 budget includes a record level of capital investment and measures to promote rural development, which could help boost LCV sales.

On the negative side, sales could continue to be disrupted by abnormal weather, a weak rupee, persistent inflation, and high interest rates. The Reserve Bank of India is not expected to start cutting interest rates soon, due to the risk of higher inflation.

Based on the weaker-than-expected September sales, we made minor downward adjustments to the 2024-25 forecasts. LV sales are still projected to reach an all-time high of 4.8 million units (+2.7%) this year and 5 million units (+3.3%) in 2025, but the risk to such forecasts is skewed to the downside.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.