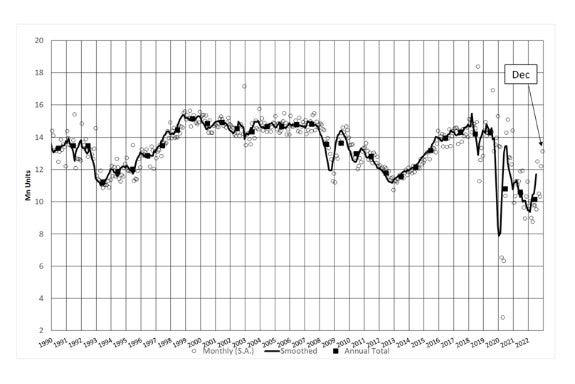

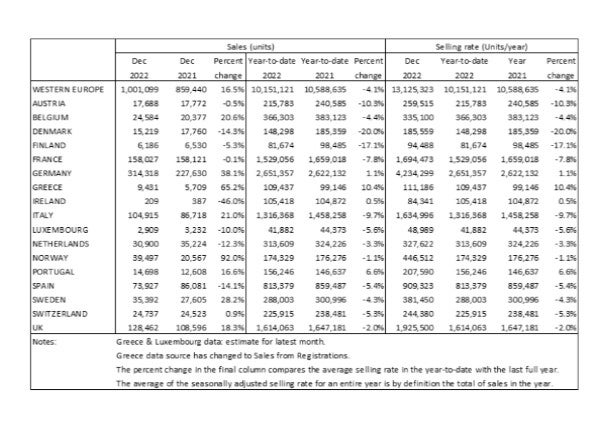

The Western Europe car market annualised rate of sales (SAAR) rose from 12.2 million units/year in November to 13.1 million units/year in December. This was the strongest performance of 2022 and was supported by a rush to register BEVs and PHEVs in some markets before government incentives changed. In raw monthly registration terms, December 2022 was up 16.5% year-on-year (YoY), with 1 million units registered. However, the overall 2022 sales volume was 4.1% lower than 2021, highlighting the intensity at which supply constraints have been hampering market performance.

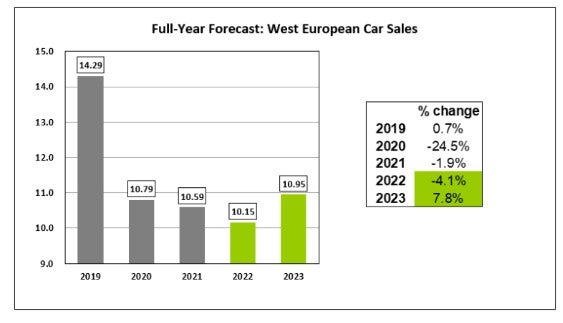

Car sales in Western Europe are estimated by LMC/GlobalData at 10.15 million units in 2022, down 4.1% on the previous year. The big markets all saw broadly flat or decreased sales of new cars in 2022. German car sales were up 1.1% at 2.65 million; the UK car market was down 2% at 1.61 million; the French market was down 7.8% at 1.53 million; Italy’s car market was down 9.7% at 1.32 million; and Spain’s car market declined by 5.4% to 813,000 units.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

With the arrival of 2023, LMC/GlobalData analysts expect supply constraints to ease, but also warn they will continue to dictate vehicle sales, with potential buyers continuing to have lengthy wait times for new cars.

Moreover, despite underlying demand having been well above what OEMs can supply (as evidenced by order backlogs), demand conditions themselves are worsening as Western Europe moves into a recessionary period over the first half of 2023. Households continue to face the squeeze of higher prices and increased financing costs, which will affect their appetite to purchase big ticket items. As such, there is a growing risk that with a worsening macroeconomic outlook, the weakening demand side will soon begin to influence vehicle sales.