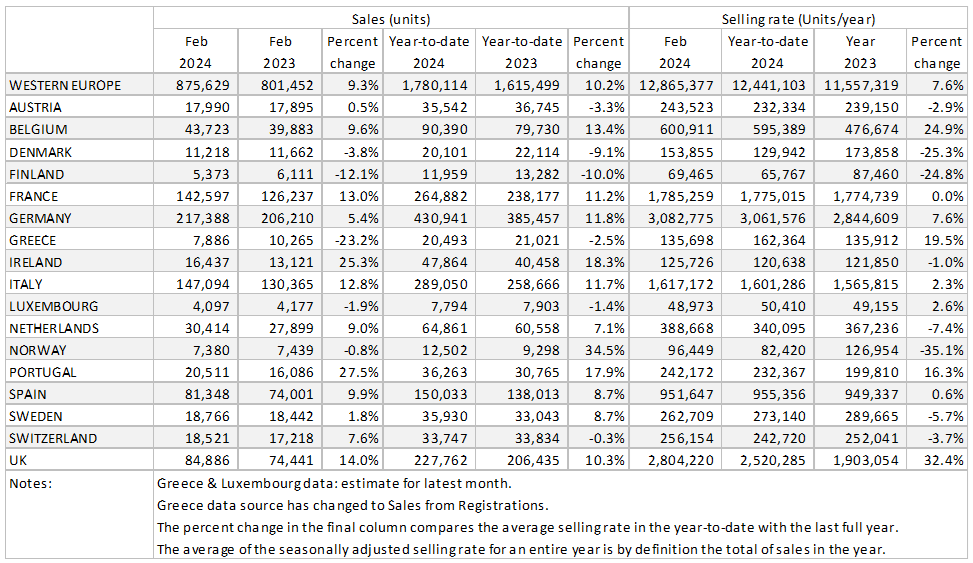

The Western Europe PV selling rate rose to 12.9 million units/year in February, with 876k vehicle registrations.

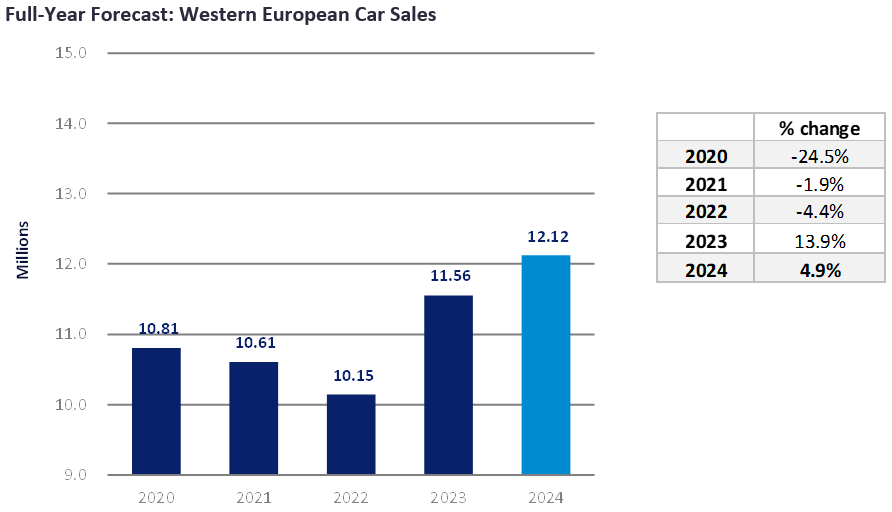

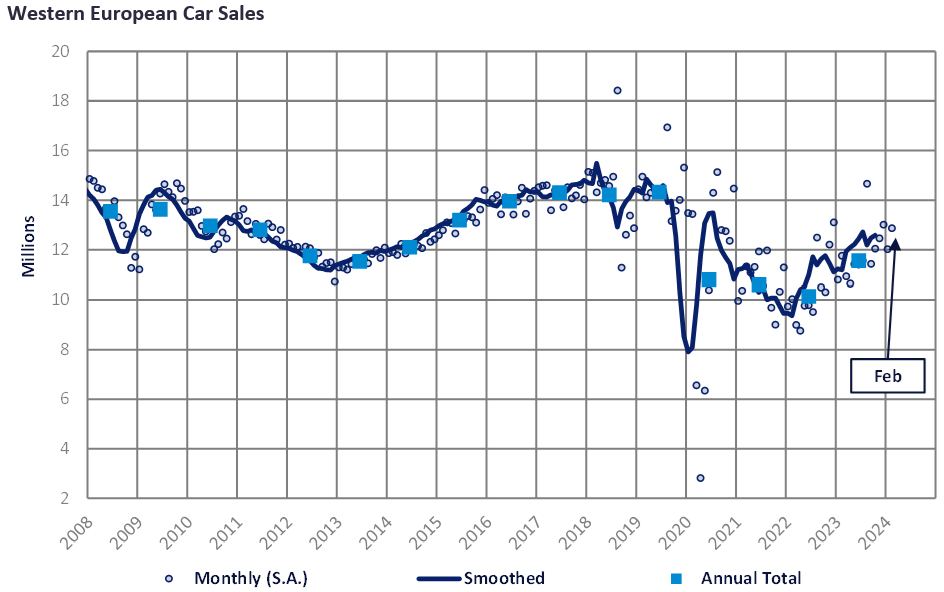

Compared to 2023, February grew by 9.3%, helped by strong year-on-year (YoY) growth in France and Italy, along with solid improvements in other major Western European countries. However, compared to pre-pandemic February 2019, the PV market is down almost 15%. The market is forecast to pass 12 million units in 2024, the highest total since the onset of the pandemic.

The German PV market performed well in February with 217k vehicle registrations, 5% higher YoY. Year-to-date, Germany has made good progress though early 2023 was a weak base for comparison given the government’s lowering of incentives on xEVs from the start of last year. The other major West European countries also performed well YoY thanks to a more supportive supply environment.

We continue to forecast growth this year, even though the macroeconomic outlook appears mixed across the region. For now, at least, households continue to face high interest rates and elevated vehicle pricing. However, with supply issues fading, we see pricing as likely to ease over the course of the year. Geopolitical risks could yet challenge this outlook, either directly through some form of supply disruption, or more broadly through keeping inflation elevated and slowing interest rate cuts.

The latest selling rate for Western Europe rose month-on-month to 12.9 million units/year. That is well ahead of January and indeed ahead of the full-year outlook. Although this indicates the potential for more optimism, seasonality is playing a part here. In the UK market, February is generally a weak month before the new registration plate number in March, so even though the market appears to have done well, in absolute volumes terms, its contribution to overall regional sales has been modest. At a regional level, Western Europe volumes for last month still look weak (-15%) compared to February 2019.

Germany’s PV market grew 5% YoY in February. The selling rate stood at 3.1 million units/year, which is the third 3 million+ selling rate in a row — however, the Germany economic outlook for the year appears tough and we are sceptical that the double-digit percentage growth of the market will continue for the full year. Meanwhile, Spain has seen selling rates slow a little at the start of this year, even though the market is comfortably up in YoY terms (+10% for February).

The French PV market achieved 142k vehicle registrations in February 2024, 13% higher than February 2023. The selling rate picked up slightly compared to January, reaching 1.8million units/year. The market is forecast to finish 2024 at 1.9million – higher than 2023, but still below the 2019 total. Italy’s PV market registered 147k units in February 2024, 13% higher than February 2023. The selling rate reached 1.6m units/year. Again here, the easing of supply constraints should see underlying demand dictate sales in 2024.