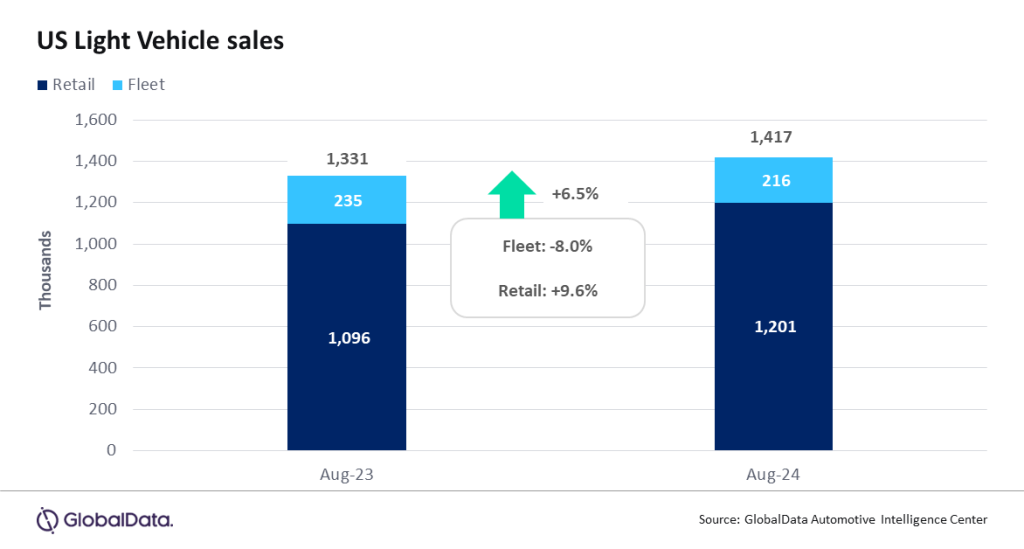

According to preliminary estimates, Light Vehicle (LV) sales grew by 6.5% year-on-year (YoY) in August, reaching 1.42 million units. This year, the month included the Labor Day weekend, according to the industry calendar, which brought about 28 selling days – the most of any month this year. This created favorable conditions for August’s growth.

US LV sales totaled 1.42 million units in August, according to GlobalData. The annualized selling rate for the month was 15.1 million units/year, down from 16.0 million units/year in July. The daily selling rate was estimated at 50.6k units/day in August, down from 51.4k units/day in July. Expectations were high coming into the month, given the inclusion of Labor Day in August for the first time since 2019. A strong seasonal factor therefore kept the annualized selling rate in check, and there is a sense that volumes could have been higher, despite positive headlines around YoY growth. According to initial estimates, retail sales totaled 1.20 million units in August, while fleet sales finished at 217k units, accounting for 15.3% of total volumes.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

General Motors was once again the leading OEM in August on 238k units, with the challenge from Toyota Group being hindered by stop sales orders on the Toyota Grand Highlander and Lexus TX. Nevertheless, Toyota Group recorded sales of 198k units, comfortably ahead of Ford Group on 176k units. At a brand level, Toyota returned to the top of the rankings, having been unseated by Ford in July. Toyota recorded sales of 169k units, around 2k ahead of Ford, while Chevrolet came in third on 154k units.

There has been something of a reversal of fortunes over recent months, with the Ford F-150 reasserting itself as the nation’s leading LV, while the Toyota RAV4 has receded from the top spot that it occupied for four of the first six months of the year. The RAV4 is likely being restrained by inventory shortages. In August, the Ford F-150 recorded sales of 40.3k units, ahead of the Honda CR-V on 38.5k units, while the Toyota RAV4 ranked third on 35.1k units. This was the first time that the CR-V outsold the RAV4 since April 2023.

Compact Non-Premium SUV was the leading segment once again in August, with its market share of 20.7% being the highest it has achieved in four months. Midsize Non-Premium SUV also saw an improvement in market share in August, reaching 15.6%, compared to 14.9% in July. Large Pickups accounted for 13.5% of the total market in August, a return to more moderate levels after two consecutive months of shares of around 14%.

David Oakley, Manager, Americas Sales Forecasts, GlobalData, said: “August had long been earmarked as a potential bumper month for the auto industry, given a calendar that had not been seen since 2019. However, comparing August 2024 with the same month five years ago demonstrates that the market is still far from fully recovered, as sales were 222k lower than in August 2019. Although the industry as a whole is seeing higher incentives than has typically been the case in recent years, there appeared to be relatively few additional deals available for the Labor Day weekend, which may have held back August sales to some extent. Consumers will be keenly awaiting the Federal Reserve’s widely-anticipated interest rate cut in September, as high financing costs have been one factor inhibiting activity in the auto market this year. Still, tighter lending criteria, recalls, and low inventory on certain models are also acting as headwinds to sales”.

US inventory levels are expected to rise slightly in August with volumes projected to be up by 1.0-1.5%, as demand cools for the third month in a row. Days’ supply is expected to be in a similar range as last month at 52-54 days. Production levels have also started to even out and August is expected to be the fourth month in a row of YoY contraction. There remains elevated risk for a further pullback in production levels as 2024 closes out.

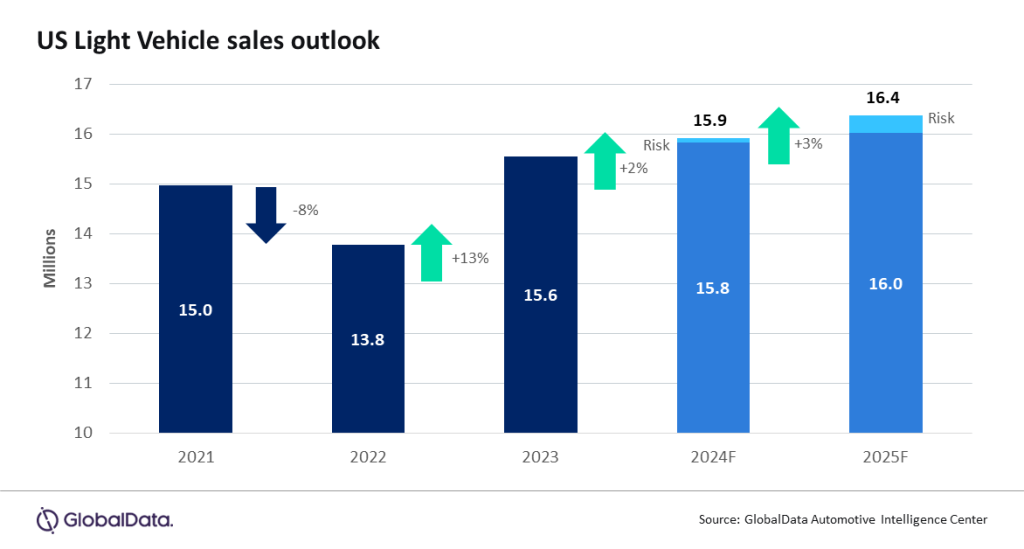

The pullback in the daily selling rate during the last three months has negatively impacted the 2024 outlook for US LV sales. The forecast has been cut to 15.9 million units, representing a 2.3% increase from 2023. Fleet sales are projected to grow by 4% in 2024, outperforming the 2% growth in retail demand. The outlook for 2025 has also been adjusted downward to align better with the current market conditions and elevated pricing. The forecast for 2025 now stands at 16.4 million units, a reduction of 200k units from our previous forecast.

Jeff Schuster, Vice President Research and Analysis, Automotive, said: “Signals indicate that US sales are losing momentum and we do not expect any measurable uptick in the daily selling rate in the coming months. Consumers who were displaced from the new vehicle market during the pandemic are still facing challenges in managing affordable monthly payments and many have yet to return. While some pricing improvements are expected for the remainder of 2024 and into 2025, they are not anticipated to occur at the previously expected pace. Without the return of entry-level buyers, sales growth is expected to flatten out over the next two years”.

Global outlook: The global LV sales rate reached just under 90 million units in July, with a slight increase of 200k units from June to 89.9 million units. While demand in the month remained healthy, it fell short of the 92.2 million units recorded in July 2023. Sales volume has now decreased for the second consecutive month, with July 2024 seeing a 1.6% decline compared to the previous year. Year-to-date (YTD) sales through July showed a 1.7% increase from YTD July 2023, totaling 49.3 million units. Performance across key markets was mixed, with the inventory recovery from last year fueling demand and creating challenging comparisons. The domestic market in China suffered the largest decrease, dropping by 10.3% from July 2023. Meanwhile, India (-3.3%), Korea (-2.8%), and Western Europe (-0.7%) also experienced declines in July. Among the volume markets, only Eastern Europe (+8.5%) and Japan (+6.7%) showed growth. The forecast for sales in 2024 remains at 88.7 million units, indicating a 2.2% increase from 2023. However, there is increasing uncertainty as global demand may be cooling and could potentially level off for the remainder of the year, posing downside risks.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.