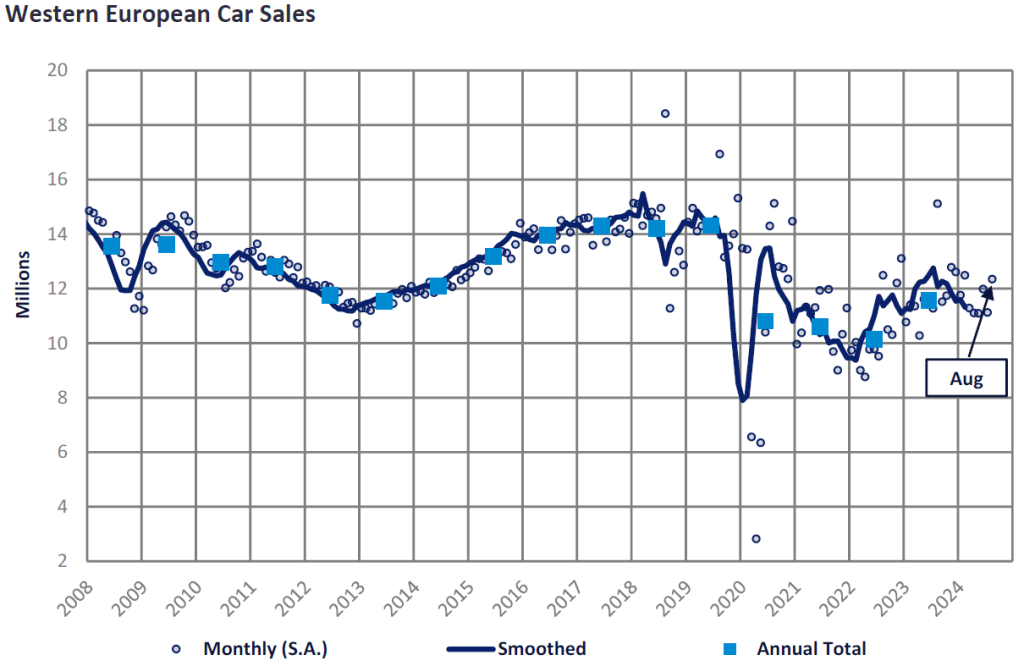

The Western Europe PV selling rate increased 10% month-on-month (MoM) in August, to 12.3 million units/year. However, it must be noted that August is a seasonally weak month for car sales, particularly in the UK, with this market having distorted the regional selling rate upward. In year-on-year (YoY) terms, sales volumes were down 18% though August 2023 was a relatively strong base for comparison as supply was improving and backlogged orders were being fulfilled.

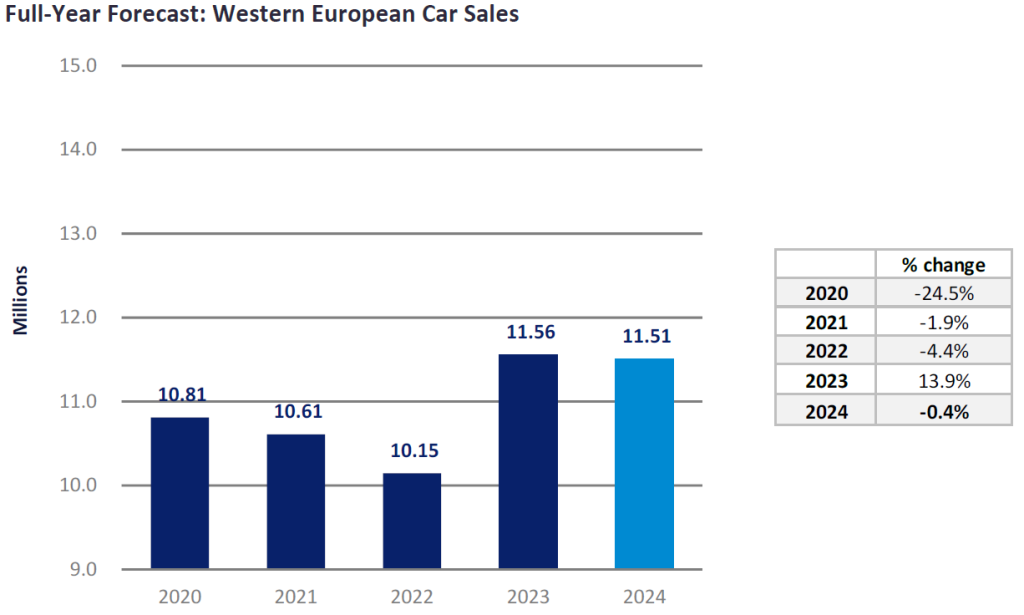

Year-to-date (YTD), the Western European market is now up by only 1%, with recent months seeing a downward trend in the YTD evolution. Political and economic issues continue to dampen consumer confidence and the overall outlook of the market in the near-term. It is evident that higher interest rates and vehicle pricing have negatively impacted sales and will continue to do so in the near-term, even if some easing of both takes place. Furthermore, the BEV market continues to struggle, causing industry leaders to call for incentivization to revive sales. We now forecast the full year result to fall just short of the 2023 total.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Commentary

The PV selling rate for Western Europe rose to 12.3 million units/year in August; however, this is an upwardly skewed result due to a stronger UK selling rate off a small base. Our growth outlook for the year has been trimmed and we now do not expect the market to pass 2023’s result. We continue to assume improved market activity in 2025 as monetary policy loosening and lower vehicle pricing come into play. Geopolitical issues, as well as political and economic uncertainty, provide downside risk.

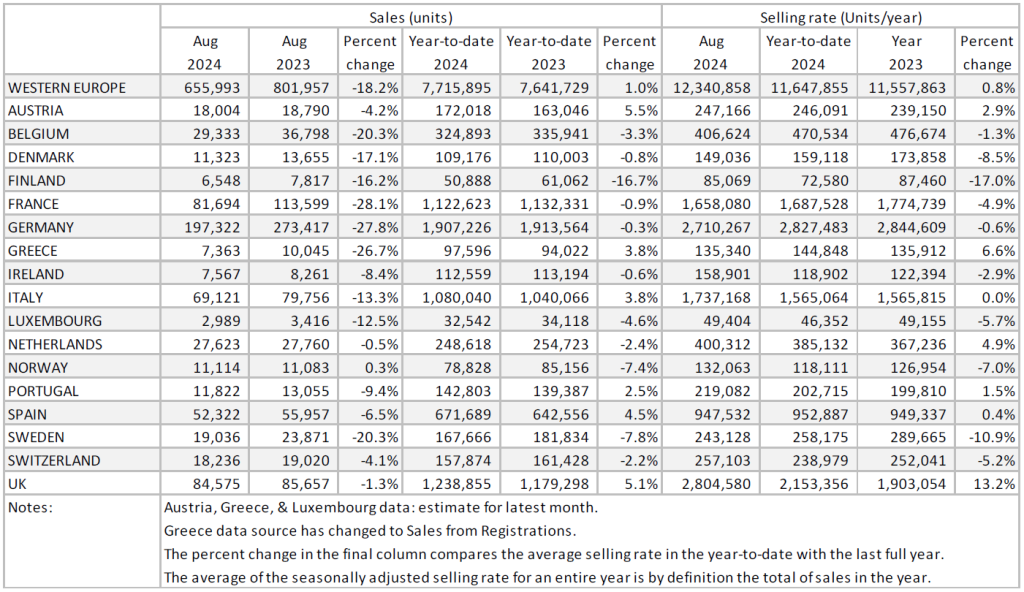

The German PV market registered 197k units in August, a 27.8% decline YoY. The selling rate fell slightly by 0.5% MoM to 2.71 million units/year. Weaker consumer confidence and a lacklustre economic picture have dragged on sales. Additionally, higher energy prices and generous subsidies in the US and China have affected the country’s industrial base. Italy’s PV market fell further in August to 69k units, a 13.3% decline YoY — this not helped by one fewer working day compared to August 2023 and high interest rates that continue to negatively affect consumers’ willingness to buy new cars. The French PV market declined by a staggering 28.1% YoY — the selling rate was flat MoM at 1.7 million units/year, though this is a poor result due to weak consumer confidence and economic data, as well as a lack of subsidies.

The UK PV market registered 85k units in August, a 1.3% decrease YoY. The selling rate increased by a staggering 31% MoM, though August is typically a quiet month, so small volume changes are amplified when converted to selling rates. Fleet continues to account for the majority of car sales as six out of 10 cars registered in August were from this sector. BEV registrations were up 11%, though remain below government targets. YTD sales have reached 1.24 million units, a 5.1% increase from the same period last year. Meanwhile, the Spanish PV market registered 52k units in August, a 6.5% decline YoY. The selling rate increased by 10% MoM to 948k units/year. Year-to-date sales are now 672k units, a 4.5% increase YoY. However, general uncertainty has affected consumers’ decision-making regarding the purchase of a new vehicle, hitting the private side of the market.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.