Reports in Japan this week suggested that Nissan Motor is ready to pull out of merger talks with its strategic partner Honda Motor, just weeks after they were announced, sending shares in the struggling automaker plunging by 6% immediately after the news on Wednesday. Whether this is a Trump-style negotiating tactic remains to be seen. Nissan’s share price has since recovered, perhaps on the news that it may be considering another, less dominant partner.

Touted as a merger of equals when it was first announced in December, it soon became clear that Nissan would very much be the junior partner in the new combined company. According to the preliminary schedule, the two automakers had agreed to delist their respective shares on the Tokyo Stock Exchange (TSE) by August 2026, after the completion of all legal formalities and new joint strategies put in place, with ownership transferred to a new holding company to have been listed simultaneously on the TSE.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

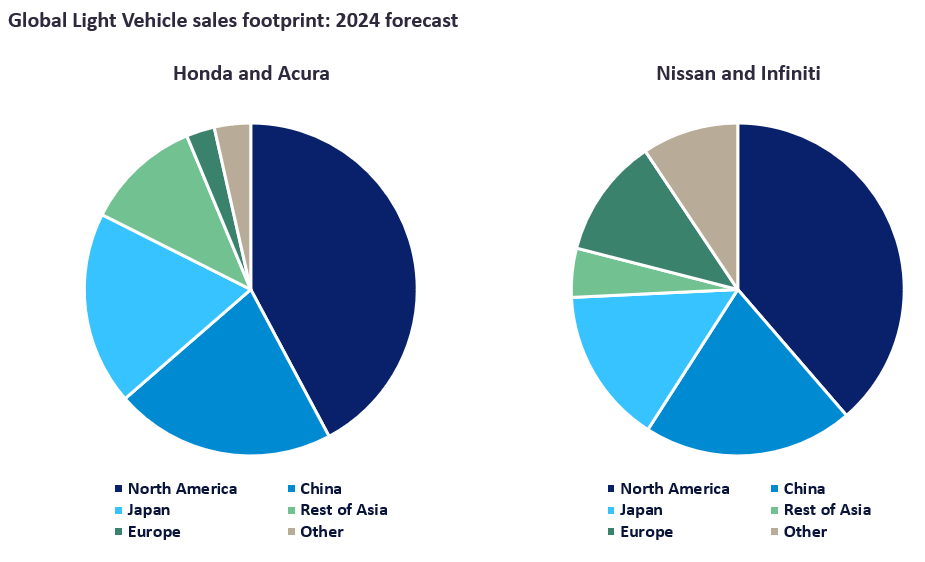

The Honda-Nissan “merger” aimed to create a new global automotive powerhouse with a combined annual output of close to seven million vehicles – behind only Toyota, Volkswagen and Hyundai-Kia. Honda and Nissan produced a combined 6.88 million vehicles last year, including 3.7 million Hondas and 3.1 million Nissans.

Such a company would be better equipped to take on the growing competition from China’s emerging global players, many of which are significantly more progressed in the transition to zero-emissions products and the development of related supply chains.

The key idea behind the merger was for the two companies to be run independently, while sharing R&D costs and supply chains to improve economies of scale – with the opportunity to develop numerous additional synergies in global markets, including capacity sharing.

The reality is that Nissan would effectively become a subsidiary of Honda, something the company is finding hard to swallow. Mitsubishi Motors, a much smaller vehicle manufacturer, has already indicated that it will decline an invitation to participate in the merger so as not to lose managerial independence.

There is significant operational overlap between Honda and Nissan, as well as substantial production overcapacity (particularly at Nissan) in important global markets, including China, Japan, North America, and Southeast Asia.

Honda’s stock market capitalization, currently at JPY 6.5 trillion (US$43bn), dwarfs that of Nissan – which is just over JPY 1.5 trillion (US$10bn). This mainly reflects Honda’s extensive non-automotive operations, including power tools and its leadership in the global motorcycle market. Separating these operations ahead of a merger would help to reduce the imbalance between the two companies, but not eliminate it entirely. Honda still produced 20% more vehicles than Nissan last year.

Honda also has a much stronger balance sheet than Nissan, although its net earnings have come under significant pressure in recent quarters due to rising competition. Since the merger was announced, Honda has also been busy showcasing its new 0-Series BEV range and its revamped “EV Hub” in the US state of Ohio, underscoring its progress in transitioning to zero-emission vehicles.

Collaboration between Honda and Nissan had already been stepped up prior to the merger announcement. Less than a year ago, the two companies jointly announced a strategic partnership in the battery electric vehicle (BEV), as they looked to accelerate their transition to zero-emission vehicles in global markets. Over the years, they have collaborated on various other projects, such as sharing research and development (R&D) costs in the development of hybrid and autonomous driving technologies and increasing economies of scale in low-volume market segments such as mini vehicles and light commercial vehicles.

There is significant operational overlap between Honda and Nissan, as well as substantial production overcapacity (particularly at Nissan) in important global markets, including China, Japan, North America, and Southeast Asia. While this means that there is significant potential to slash costs, there are early indications that, if the takeover were to go ahead, most of the cuts would be expected to be made by Nissan.

Last month, Carlos Ghosn, who led Nissan for 19 years until his ouster in 2018, characterized the proposed merger by saying, “without any doubt, Honda is going to be in the driver’s seat. There is practically no complementarity here, which means if they want to develop synergies, it is going to be through cost reduction, elimination of duplication of plants and technology development, and we know exactly who is going to pay the price. It is going to be the minor partner, and it is going to be Nissan.”

Honda’s CEO fueled these fears further last month by telling Nissan it wants it to step up its global restructuring and reduce overcapacity as a precondition of the merger. Honda seemingly was not too impressed with the plan announced by Nissan in November to cut 9,000 jobs worldwide and reduce its global production capacity by 20%.

Last month, executives from Renault SA – including CEO Luca de Meo, traveled to Japan to get involved directly in the merger talks with Honda. The French automaker is Nissan’s largest shareholder, with a 36% stake, albeit down from 44% just two years ago. As such it has a significant vested interest in Nissan, including its valuation within a merged company with Honda. Sources suggested that, at the very least, Renault would expect to be paid a takeover premium for its shares in Nissan.

Renault had more than two decades to develop a winning partnership with Nissan, but synergies between the two companies were few and far between. This has left Nissan ill-prepared for the current challenges in the global marketplace, including the transition to zero-emission vehicles and the rapid rise in competition from the Chinese auto industry.

Nissan’s chances of surviving the crucial next two years as a standalone company, without a very substantial injection of fresh capital, remain slim. It needs to undertake substantial restructuring and investment to transition to zero-emission vehicles.

A new strategic partner will be essential; perhaps one with less overlap may be the answer – such as a Chinese automaker with aggressive overseas expansion plans. Renault, in recent years, has been nurturing a deepening partnership with Chinese automaker Zhejiang Geely Holding Group and plans to continue to sell down its stake in Nissan in any case, after relations with Nissan became strained following the ouster of Carlos Ghosn over five years ago.