At a macro level, the year 2024 brought a small increase in global vehicle sales, but it was a decidedly mixed picture and the year was dominated by the underlying theme of a sector in fundamental transition, with much uncertainty ahead. It was also a year in which the bumpy nature of the transition had consequences for companies who found themselves resetting plans, especially in the face of slower than expected electric vehicle sales.

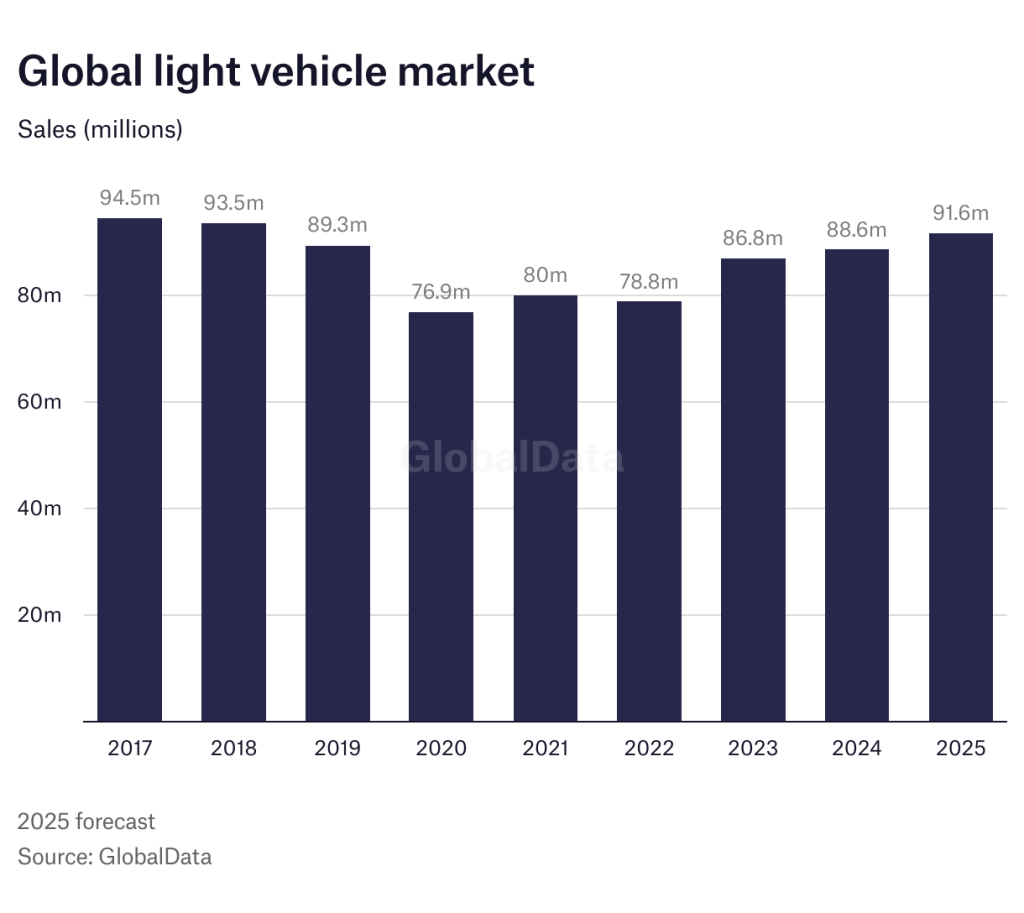

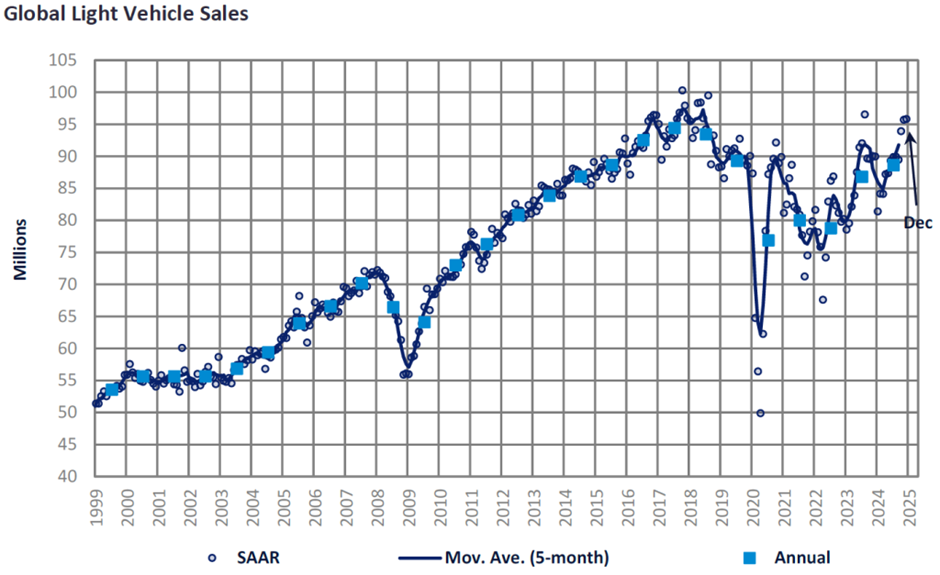

First, the overall picture. The global light vehicle market in 2024 laboured to register unspectacular growth of 2% at around 88.6 million units. Market trends were mixed in the major regional markets of the world.

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

The US vehicle market was a strong positive on the back of an economy that continued to surprise on the upside. China was subject to a price war which supported sales volumes but at the expense of profit margins for most companies. Europe’s market continued to disappoint, its performance hampered by a weak economy overshadowed by elevated levels of public debt, high interest rates and the negative confidence impacts resulting from the war in Ukraine.

Forecasts for the global vehicle market over the next few years see growth, but it’s a rather modest upturn by historical standards, subject to significant downside risk.

The last peak for the global light vehicle market saw it hit 94.5 million units in 2017. A major downturn in the early 2020s caused by Covid 19 saw the market plunge to under 80 million units a year. Following the pandemic, subsequent supply shortages emanating from the global ‘chips crisis’ constrained the industry’s recovery from that low point.

In 2025, GlobalData forecasts the global light vehicle market at 91.6 million units, some 3.4% ahead of 2024’s estimated 88.4 million.

Much remains uncertain as we look at 2025. Political developments in the US threaten bigger and broader US trade tariffs generating downside risks for global trade, investment and wider economic growth across the world.

Vehicle pricing and the level of required demand management in Europe and North America – but also India and elsewhere – will again be key for volume growth moving through 2025. Although the timing, scale and scope of potential trade obstacles associated with the Trump presidency remain uncertain, downside risks are an ongoing concern.

However, the positive impact of lower interest rates, new model activity and competitive pressures underpin GlobalData’s modest sales growth forecast for 2025. That said, the challenges for the sector remain considerable, especially in the ongoing energy transition – still at an early phase – and the wider impact of the competitive threat from China.

For 2025, a demand-led boost in China from confirmed NEV subsidies struggles to offset softer assumptions for the demand environment in both Europe as well as North America.

What about prospects for 2025 sales in the three major markets – the China, the US and Western Europe?

China’s price war intensifies

Competition in China’s battery electric vehicle (BEV) segment continued to be ramped up in 2024, with new brands coming onto the market and new models launched on a weekly basis. The more dominant manufacturers have been discounting heavily to buy market share, while the smaller start-up companies have struggled to keep up.

For all the heavy discounting, increased government incentives, and improved availability of finance, Chinese BEV sales growth was sluggish in 2024 – by recent standards. While global sales of Chinese-made new energy vehicles (NEVs are BEVs and plug-in hybrids) soared by 36% to 11.262 million units in the first eleven months of 2024, according to wholesale data compiled by the China Association of Automobile Manufacturers (CAAM). Most of this growth has come from plug-in hybrid electric vehicles (PHEVs).

Chinese consumers are taking advantage of scrapping subsidies and massive price cuts, as the price war, which appeared to be winding down in late 2023, regained momentum in 2024. A sign of the pressures: leading car maker BYD is asking suppliers to cut prices further. The brutal price war will likely intensify in 2025.

To help maintain the momentum in the market, the government has extended the scrapping subsidy program until the end of 2025 and also expanded the type of vehicles that qualify for the subsidies. In addition, the sales tax exemption for NEVs remains effective until the end of this year. As such, sales are expected to remain buoyant this year, led by strong NEV sales (which outsold ICEs in the Passenger Vehicle sector in H2 2024). Yet, global uncertainty and the still depressed property market present risks to the economy and the automotive market.

Further, most economists see China’s economy on a structural downturn – caused by demographics and diminishing returns to capital – compounded by current imbalances in the property sector that are spilling over into broader financial instability and investment climate uncertainties. China’s light vehicle market grew by an estimated 0.9% to 25.5 million units in 2024. Incentives and continuing highly competitive conditions are forecast to take the Chinese light vehicle market to 26.8 million units in 2025. However, the world’s biggest vehicle market will continue to struggle with weak underlying demand and a sluggish economy.

One footnote on government scrapping incentives: China’s domestic market decelerated sharply in January, despite the apparent extension of the scrapping subsidy program, which was originally set to expire at the end of 2024. Preliminary data indicates that, after adjusting for holidays, the January selling rate was estimated to be only 24.5 million units a year, a 14% decrease from a solid December. In year-on-year terms, sales declined by about 1% in January, although sales a year ago were also weak. The government announced the extension of the scrapping subsidies on 8 January, but it is reported that the programme was not available to consumers in about half of the country’s provinces before the Lunar New Year holiday. This likely contributed to the slowdown in sales, particularly for NEVs, which benefit most from the incentive programme.

US market strong, despite political uncertainties

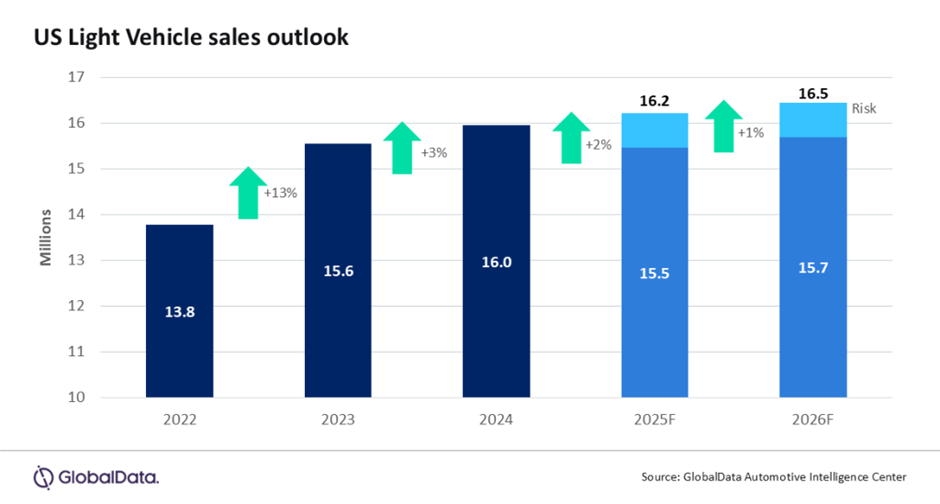

A strong US economy propelled the US market to growth in 2024, despite considerable uncertainty ahead of the outcome of November’s US presidential election. After the election, considerable uncertainty remains over the future direction of the Trump administration’s policies and capabilities to enact policies into law. Those uncertainties – particularly on areas of trade and investment rules – could significantly impact both the US economy and the automotive sector.

In the US marketplace, buoyant demand following the easing of supply constraints meant transaction prices stayed high in 2024, which was largely good news for the OEMs in terms of levels of profitability. However, there are some concerns that consumers may increasingly hold off on purchases due to affordability issues or the expectation that interest rates will come down later in 2025.

With Donald Trump winning the US presidential election, automotive-specific policy could be reshaped, including in the areas of EV tax credits, emissions standards, and autonomous vehicle regulation. Implementing policy surrounding EV tax credits will require Congressional action, so could take time to push through, analysts say. There is also the big question of where the next Trump administration will take import tariffs on many products, including vehicles – and which countries or trade blocs will be targeted. High tariffs would likely result in a generalised impact on prices of imported vehicles and components that would also spill over to higher costs for domestic producers.

In 2024 the US light vehicle market is estimated at around 16.0 million units, in the end a modest 2.6% gain on the previous year. It is forecast at 16.2 million sales in 2025, but vehicle pricing is likely to remain robust on the back of more technology, electrification costs and lower inventories.

In terms of the automotive industry forecast, GlobalData analyst Jeff Schuster highlights the potential impact of tariffs. “The outlook for US auto demand hinges on the scale, extent, and duration of import tariffs that are being considered by the Trump administration,” he says. “Negative implications could be significant, with up to one million units of demand potentially at risk in the US alone. Retaliatory measures would significantly raise global risks and escalate the situation to a full-fledged global trade war, disrupting the current momentum in the auto industry. Ultimately, consumers stand to lose the most.”

Europe’s car market sluggish in 2024 – and will stay that way in 2025

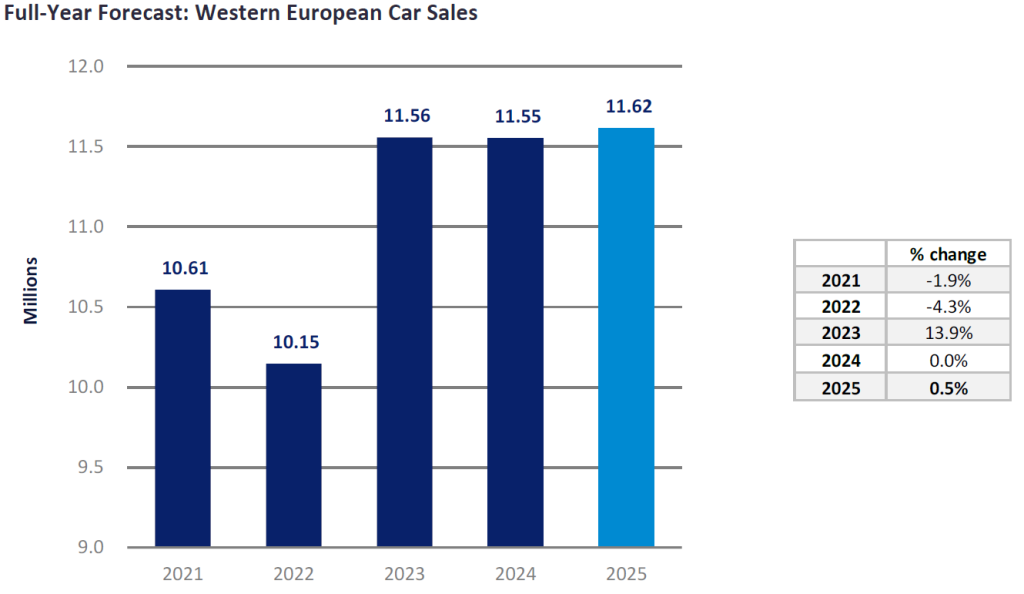

In the latter months of 2024, Western Europe’s car market picked up from a low running rate, but sales in the year were flat on the previous year at around 11.55 million. Political uncertainty in Germany and France, both countries grappling with high levels of fiscal debt and struggling automotive sectors, has added to the challenges facing the region. Pricing remains a cause for concern, even though the economic situation is slowly moving in the right direction for consumers as interest rates ease. However, the ramping up of tariffs proposed by President Trump risks hampering the European economy.

Pricing remains high in Europe, and with OEMs struggling in the face of a price war in China, and likely increased price pressures in the US from new tariffs, carmakers will do their best to retain high pricing in Europe going forward. That said, there are some positive factors when considering affordability. The ongoing reduction in interest rates is certainly helpful for vehicle financing; meanwhile, more affordable vehicles are being ramped up this year. However, these factors will not drastically change the high pricing environment.

The outlook for 2025 is now more subdued because of the growing concerns over international trade and the strength of the overall economy. Among key global markets, Western Europe looks set to remain the biggest laggard by far in terms of recovery versus pre-pandemic. Western Europe’s car market last peaked at 14.3 million units in 2017 before plummeting to under 11 million units a year through the pandemic and its after-effects (supply shortages).

Globaldata analyst Jonathon Poskitt neatly puts the industry’s current situation in perspective. “Look, it’s been a growth trajectory for global sales since the lows of a few years ago and the whole industry has to be grateful for that – of course. But there are issues with transaction prices and affordability as well as a pretty brutal price war in China.

“Furthermore, serious geopolitical concerns are very much front of mind for many and there are real risks associated with rising trade protectionism and what that potentially means for the global economy. With its international operations, the auto industry feels these things – potential headwinds – very acutely.

“At the same time, manufacturers also have to navigate the energy transition and maintain competitiveness in new advanced technologies, which tend to be expensive. Investment strategies have never been subject to such complexities. It’s a lot to deal with in terms of both corporate strategies and shorter-term operational priorities.

“The reduced size of the overall demand pie is not exactly helping. For Western Europe, a forecast market of 11.6 million units in 2025 is pretty disappointing when seen in the context of what was a ‘normal’ car market not so long ago.”