In recent months, Thailand’s automotive landscape has undergone a monumental transformation with the entry of two formidable Chinese EV giants, GAC Aion and Changan. They follow in the footsteps of BYD, the world’s leading electric car manufacturer, which made its foray into the Thai EV market just last year. As these newcomers explore the advantages and prepare to partake in Thailand’s incentives package, the country is already hosting a total of 23 promoted projects involving 16 different OEMs in electric vehicle production, with an investment value of 75,141 million THB, and an EV production capacity of 710,000 units, positioning Thailand as the leading manufacturing hub for EVs in ASEAN.

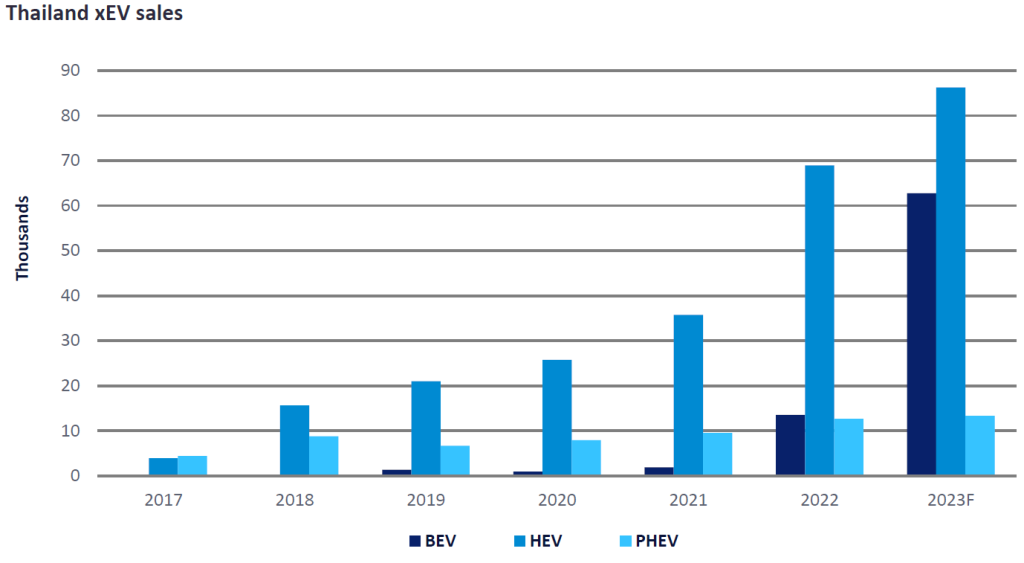

The journey began in 2017, a time when pick-up trucks and eco cars reigned supreme as the country’s product champions. However, with the global shift towards electrification, the government set its sights on embracing the EV wave as a new S-curve product and unveiled ambitious plans that included the introduction of hybrid, plug-in hybrid (PHEV), and battery electric vehicle (BEV) incentive programmes that offered corporate income tax (CIT) reduction and excise tax benefits.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The BEV odyssey began in late 2018 when Nissan unveiled the Leaf, followed shortly by the launch of the MG ZS EV in early 2019. Despite a tempting array of incentives, the adoption of BEVs in the following years remained surprisingly low. The reason for this unexpected result was the stronghold of hybrids from the dominant Japanese OEMs, who claimed an impressive 90% share of the Thai market. Nonetheless, this focus on hybrids from Japanese OEMs did lead to success. Hybrid sales surged from a mere 4,000 units in 2017 to nearly 16,000 the following year, paving the way for other EV technologies to follow suit.

Fast forward to 2021, a pivotal year in Thailand’s EV journey. Great Wall Motors (GWM) introduced ORA, a BEV-only brand that caught EV enthusiasts’ attention. Slowly but surely, BEVs began carving out a niche, albeit a modest one. GWM’s success became a beacon and attracted more Chinese OEMs to investigate Thailand’s promising EV potential.

However, the real game-changer arrived late in 2022 when the Ministry of Finance announced the BEV subsidy package, EV3.0. This programme offered substantial incentives, including a maximum 150,000 THB (€4,000) subsidy for BEV buyers, special excise tax rates, and completely built units (CBU) import tariff reductions. Combined, these benefits translate to a remarkable reduction of up to €6,000 in BEV prices and have led to an explosive interest from various OEMs in participating in the BEV programme. Last year, Hozon Auto debuted NETA, a Chinese brand focusing on affordable BEV models. In August 2022, China’s top-tier BEV maker, BYD, joined the ranks, creating electrifying waves across the country. Even Tesla joined in the hype later in 2022 without participating in any government programmes.

The year 2023 has marked the peak of BEV’s popularity. The Thai EV3.0 programme with its enticing incentives and subsidies has become even more appealing to Chinese OEMs. As a consequence, a growing number of OEMs have expressed their desire to enter the Thai market. Leading players such as GAC Aion, Changan, Chery, JMC, and several others seized the opportunity and promptly initiated consultations with Thailand’s Board of Investment (BOI) to explore investment prospects.

The Thai government has successfully secured contracts with BYD, Great Wall Motors, SAIC-MG, NETA, Toyota, and Mercedes-Benz, all committed to investing in and locally manufacturing BEV vehicles. This initiative has undeniably achieved remarkable success in boosting BEV sales in the Thai market. Between January and August 2023, a total of 42,502 BEVs were sold in Thailand, with expectations that the year will close with over 62,000 BEV sales.

As the EV3.0 subsidy is set to expire by the end of 2023, the Thailand EV Board has prepared the next subsidy package, EV3.5, and proposed an extension of the subsidy with a new budget for 2024-2025. While the tax incentives in EV3.5 mirror those of EV3.0, the subsidy amount per BEV will be reduced to a maximum of 100,000 THB. As a result, the growth rate in 2024 may not match that of 2023, but sales will continue to grow as the BEV ecosystem matures, and more charging stations are built.

Yet, amidst all this promise and potential, questions linger. What lies on the horizon for Thailand’s evolving EV landscape? Will Chinese OEMs dethrone the Japanese giants? Can Thailand achieve its ambitious “30@30” EV vision, which aims for 30% of car production to be zero emission vehicles (ZEVs) by 2030? The story is far from over, and the world eagerly awaits the next chapter in this electrifying journey.

Kunat Tharasrisuthi, Manager, Asia Powertrain Forecast, GlobalData

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center