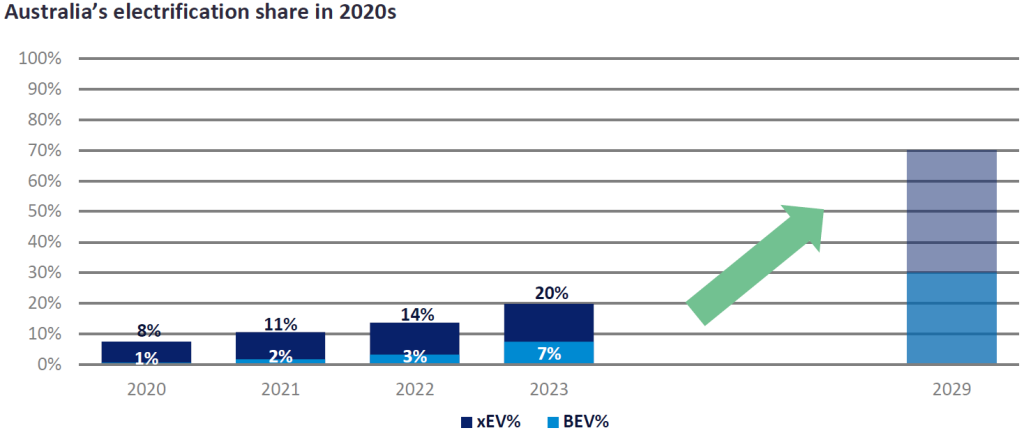

Australia is emerging as a key player in the shift to electrification in the Asia-Pacific region, particularly in the Battery Electric Vehicle (BEV) segment. With federal and state-based incentives, the country is poised to grow its xEV market significantly. In 2023, Australia achieved the fifth largest xEV sales share in the Asia-Pacific region, the technology accounting for approximately 20% of Australia’s Light Vehicle (LV) sales. Additionally, Australia recorded the fourth largest BEV sales in the Asia-Pacific region, with a target of reaching 100% Zero Emission Vehicles (ZEV) by 2050.

To accelerate this transition, the Australian Government passed legislation for an Australian New Vehicle Efficiency Standard (NVES) in May 2024, which will take effect from January 2025. The NVES will establish average CO2 emission targets for each automotive brand. The average CO2 emissions target for Passenger Vehicles (PVs) must be less than 141 g/km.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Manufacturers will earn credits for achieving lower CO2 emissions than the established targets but will face penalties for exceeding the limits. A fine of AU$100 (US$66.50) will be imposed for every gram of CO2 per kilometre that exceeds the threshold for each vehicle sold. If a manufacturer fails to meet the target, they will have a two-year grace period to rectify the situation before facing monetary penalties. They can either generate credits or purchase excess credits from other manufacturers.

The NVES aims to reduce CO2 emissions by 60% by 2029, with targets set at 58 g/km for PVs. This policy is expected to transform the landscape of vehicle types in Australia significantly. In an ideal scenario where no manufacturer incurs penalties, more than 75% of PV sales in Australia will need to be xEVs, predominantly PHEVs or BEVs.

It will be interesting to see which strategy each brand adopts to meet this policy. Traditional manufacturers with high sales volumes and a significant reliance on Internal Combustion Engine (ICE) technology face considerable challenges in rapidly transforming their offerings to meet these targets. These brands are expected to initially lean towards hybrid electric vehicle (HEV) technology while enhancing their BEV technology and offerings by the end of the decade. PHEVs could also assume a more vital role, particularly in the mid to large vehicle segments, to significantly lower emissions in lieu of BEVs.

Conversely, xEV-only manufacturers such as Tesla and BYD are well-positioned to comply with the emission targets and may benefit from selling excess credits. This policy could also create opportunities for new xEV brands to enter the market.

Nevertheless, it is reasonable to anticipate that some brands will find it challenging to meet the emission targets and may choose to purchase surplus credits or accept penalties.

In summary, the NVES policy is anticipated to accelerate electrification in Australia significantly, positioning the country as one of the leading xEV markets in the region. As the automotive landscape evolves, the focus on reducing emissions will drive innovation and transformation within the industry.

Methin Changtor, Senior Manager, Asia Powertrain Forecasts, GlobalData

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.