Stellantis has released its Q2 2026 estimated consolidated shipments.

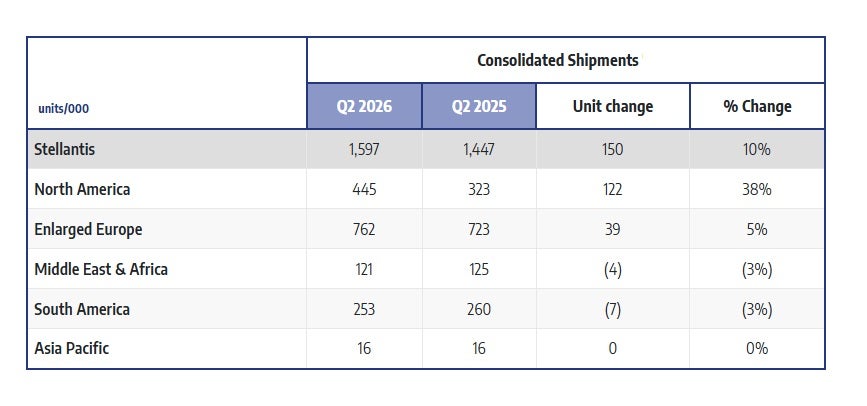

It said consolidated shipments for the three months ended June 30, 2026, were an estimated 1.6 million units, up 10% year-over-year. Growth was driven primarily by North America and Enlarged Europe, partially offset by lower volumes in the Middle East & Africa, largely due to the regional conflict, and in South America, where a weaker Argentine market weighed on performance.

In North America, Q2 shipments increased by approximately 122k, or 38% year-over-year. Stellantis said the majority of the NA growth was driven by new or refreshed products and powertrain offerings, including the Ram 1500 (light-duty) HEMI V8, the new Ram 1500 TRX SRT, the refreshed Jeep Grand Wagoneer and Grand Cherokee, and the refreshed Chrysler Pacifica. There is also a continued ramp-up of the new Jeep Cherokee and Dodge Charger 2-door and 4-door SIXPACK. It also reflects preparations for the planned summer production shutdown.

In Enlarged Europe, Q2 shipments increased by approximately 39k, or 5% year-over-year, supported by higher industry volumes. Growth came from both Stellantis- and Leapmotor-branded vehicles, with BEV shipments serving as the primary driver, the company said. For Stellantis brands, shipment growth was driven primarily by recent product launches. Strong demand for Smart Car platform nameplates including the Citroën C3 and C3 Aircross, Opel/Vauxhall Frontera, and Fiat Grande Panda, contributed approximately 41k additional units, representing 51% growth year-over-year. In the C-segment, the new Jeep Compass also contributed positively, adding approximately 8k units. These gains were partially offset by an approximately 28k decline in shipments of legacy B-SUV models, including Jeep Avenger, Fiat 600, Opel Mokka and Peugeot 2008.

Leapmotor-branded vehicle shipments increased by approximately 25k units to 33k, driven by ‘strong demand’ for the T03 and the B10.

In Middle East & Africa, shipments declined by approximately 4k units, or 3% year-over-year, reflecting the impact of the regional conflict. Growth in the region was supported by Algeria, up approximately 8k units, from the continued ramp-up of the Fiat Doblo and, to a lesser extent, higher shipments in Morocco driven by stronger industry volumes. These gains were more than offset by Türkiye, down approximately 8k units, amid weaker market conditions, and shipments in Gulf Cooperation Council countries, which declined by approximately 50%.

In South America, shipments declined by approximately 7k units, or 3% year-over-year. The growth in Brazil, up approximately 21k units, supported by ‘favourable industry conditions’, was more than offset by lower shipments in other markets, mainly in Argentina, where shipments declined by approximately 25k units.