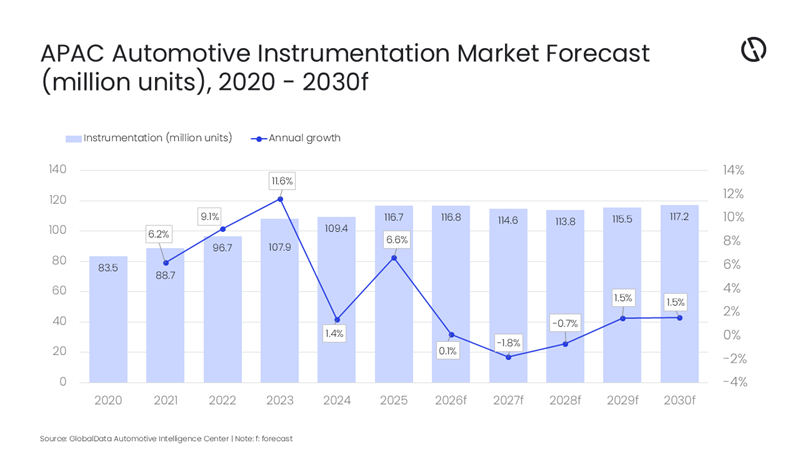

The Asia-Pacific (APAC) automotive instrumentation market continues to evolve as vehicles become more digital and software-led. While the regional growth outlook appears modest over the coming years, APAC remains an important centre for cockpit innovation due to its scale in vehicle production, ongoing electric vehice (EV) adoption, and steady consumer interest in safer and more connected in-cabin experiences. Against this backdrop, the APAC automotive instrumentation market is projected to grow at a compound annual growth rate (CAGR) of 0.1% between 2025 and 2030, according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s latest report, “Global Sector Overview & Forecast: Automotive Instrumentation Q1 2026”, reveals that the APAC automotive instrumentation market is poised to grow from an recorded volume of 116.7 million units in 2025 to 117.2 million units in 2030.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

Madhuchhanda Palit, Automotive Analyst at GlobalData, comments: “APAC demand for modern instrumentation is being supported by practical trends rather than hype: increased penetration of driver assistance features, rising familiarity with digital interfaces, and automakers’ push to modernize cabins to remain competitive. Even in a slower-growth environment, instrumentation remains a highly visible area where OEMs can refresh models and improve perceived value without redesigning the entire vehicle.”

China continues to play a central role in APAC’s cockpit direction, supported by its EV ecosystem and fast implementation cycles for connected features. This environment encourages experimentation with new display formats, integrated cockpit layouts, and software-centric user experiences. India, while different in price sensitivity and feature mix, is still moving toward more advanced clusters and infotainment-led cockpits as passenger vehicle production expands and buyers increasingly expect modern screens and smartphone-like usability. Japan and Korea remain important as technology and quality benchmarks—particularly for premium implementations of HUDs and advanced dashboard design—though their influence is often expressed through refinement and reliability rather than volume-driven disruption.

Palit adds: “A key shift across APAC instrumentation is the gradual move from component-based cockpit design to more centralized, software-driven architectures. Domain controllers and zonal approaches—most notably discussed in the context of China—can simplify integration between the instrument cluster, infotainment, and connected services. Over time, this can help OEMs roll out updates more efficiently and offer more consistent user experiences across model lines.”

Palit concludes: “APAC’s automotive instrumentation market is expected to progress steadily rather than surge, but it remains strategically important to the global cockpit roadmap. The next phase is likely to be defined by incremental upgrades: more integrated digital clusters, broader HUD availability, and a continued shift toward software-led cockpit management. For the APAC automotive sector, the opportunity may lie less in rapid market expansion and more in consistent execution—delivering safer, clearer, and more connected driver interfaces while keeping complexity and cost under control.”