Car registrations rose 17% in July, marking 12 consecutive months of positive year on year growth in Europe.

“After just over a year of monthly decline – between July 2021 and July 2022 – the market has been on a positive trajectory since August 2022,” JATO Dynamics said.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

In total, 1,018,403 new passenger cars were registered in July, compared to 873,825 in July 2022. The year to date (YTD) volume jumping from 6,460,730 units in 2022 to 7,581,537 in 2023 marked the highest result since the Covid-19 pandemic took hold.

Different fuel types played a role in the number of registrations during the month.

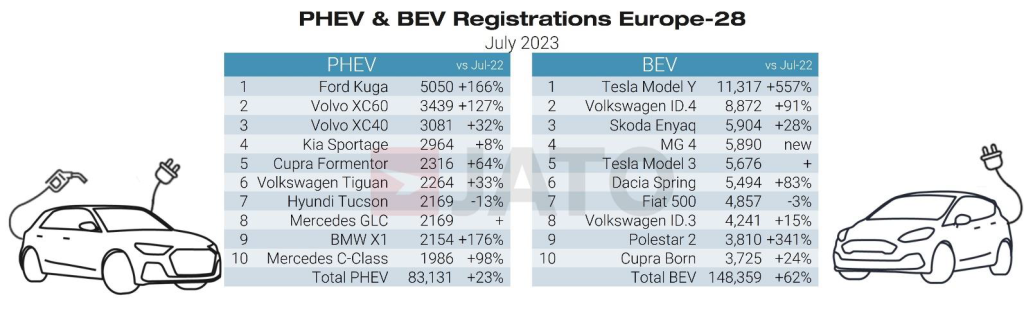

Although BEVs (battery electric vehicles) saw an increase of 62% in July, petrol cars continued to experience significant sales. Demand increased by 15% last month to 589,705 units, accounting for 58% of total cars sold in July.

Felipe Munoz, global analyst at JATO Dynamics, said: “Despite BEVs being incentivised by governments and penalties enforced for those that use certain combustion engine cars, consumers are continuing to buy the latter. Gasoline cars are being sold at a similar rate to last year with less than a percentage point difference between their market share in July 2022. It’s therefore clear that consumers still have concerns and remain reluctant to fully invest in new energy vehicles.”

Several factors account for this continued popularity, in particular, the difference in price points. The average retail price of electric passenger cars available in Germany in H1 this year was 39% higher than their petrol counterparts. A lack of available BEV models is also a key challenge with 109 BEV and 297 gasoline models on offer in Germany.

Munoz added: “The industry needs to do more if we are to see BEVs compete and succeed alongside familiar, long standing gasoline cars. Regulation alone can’t achieve this– heightened awareness and fairer prices will be required if we’re to drive greater BEV adoption.”

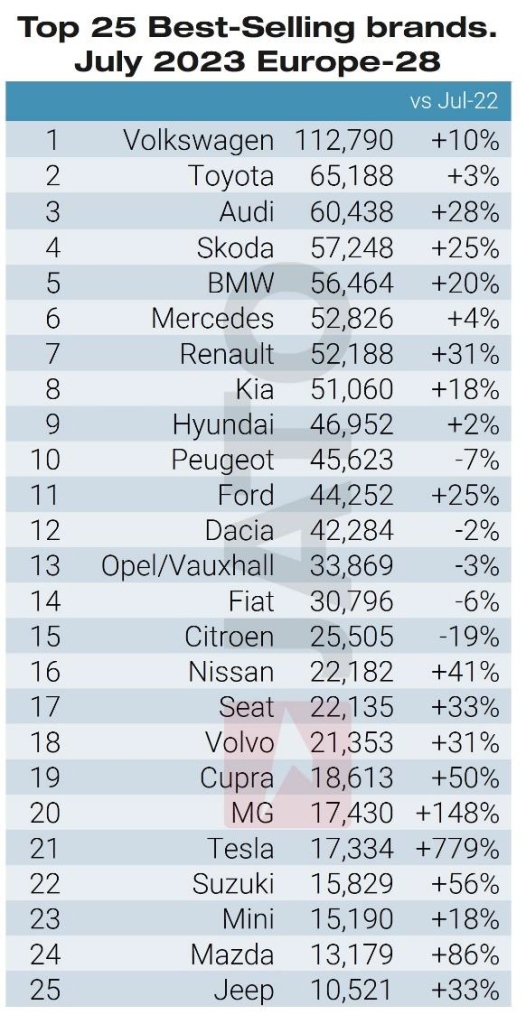

Volkswagen Group dominates

As the shift to electric continues to be the priority for the European car industry, some OEMs are using the evolving market conditions to their advantage, in particular, the Volkswagen Group. Currently, VW’s growth is primarily being driven by its ICE (internal combustion engine) and PHEV (plug-in hybrid electric vehicle) models such as the Skoda Octavia, Volkswagen Tiguan, Polo, Audi A3, and Cupra Formentor.

The VW ID.4 was the manufacturer’s best selling BEV in July. However, it only took eighth place overall during the month, and was the 13th best seller between January-July 2023.

Munoz said: “The German manufacturer gained 0.8 points of share in July, moving up to 27.49% marking its highest monthly market share in two years. It’s interesting that large OEMs – such as VW, the largest OEM in Europe – are still relying on traditional combustion engine models to spur such growth.”

In contrast, Stellantis continued to lose traction during the month, despite being the second largest European OEM. With 15.62% market share in July, the brand lost 3.5 points when compared to July 2022, and the gap in market share between VW Group and Stellantis was the largest it had been since the creation of Stellantis at the beginning of 2021.

Chinese OEMs yet to gain traction

Last month, the 22 Chinese brands available in Europe sold 25,564 new passenger cars across the region 131% more than the number registered the year prior. Over the same period, their market share doubled from 1.27% to 2.51%. However, 88% of the volume registered by Chinese manufacturers was from MG, Lynk & Co, and DR Automobiles – brands that are not positioning themselves as Chinese in origin.

Munoz said: “Reputation and brand awareness are the two biggest challenges that Chinese OEMs face, particularly in the west, and they’re very aware of that. Changing this perception will require a lot of work – more than simply offering a good product at a competitive price.”

Golf returns to the top 3

The ranking by models showed significant changes, with the VW T-Roc taking the top spot as it had done the year prior. Despite being the top model, it experienced a decrease of 5% in volume. The Dacia Sandero ranked second and remained in a similar position to July 2022, and the VW Golf took third place, the best position it has secured so far this year. Its growth was driven both by its petrol versions alongside business/fleet registrations.

Other top performers included the Renault Clio, Skoda Octavia, and Ford Puma. Among the latest models, the Austral led with 6,103 units, becoming Renault’s fourth best selling product and almost outseeing the Arkana with 6,138 units. The MG 4 was the fourth top selling BEV of the month registering 5,890 units, racing ahead of its direct competitors – Volkswagen ID.3 and the Renault Megane with 4,241 and 3,380 units respectively.

Jeep’s Avenger became its new top seller, registering almost 4,000 units. Meanwhile, BMW sold 3,461 of its iX1 model, becoming the brand’s most popular BEV. Toyota registered 2,813 units of the Corolla Cross, which was significantly lower than the Corolla volume of 11,527 units.