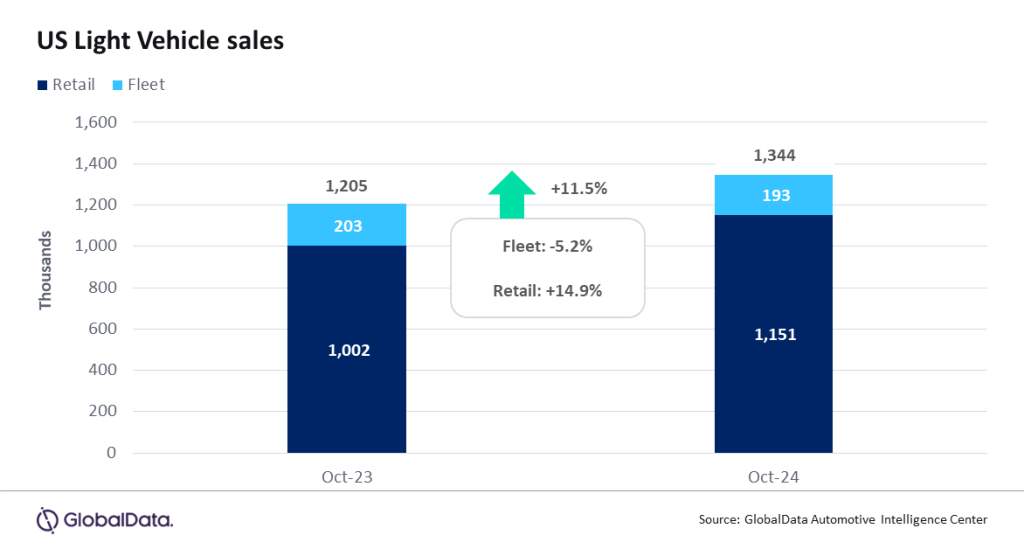

According to preliminary estimates, Light Vehicle (LV) sales grew by 11.5% year-on-year (YoY) in October, to 1.34 mn units. Although the month had two additional selling days than it did in 2023, sales still exceeded expectations and provided a more upbeat perspective on the industry than has generally been the case in recent months.

US LV sales totaled 1.34 mn units in October, according to GlobalData. The annualized selling rate for the month was 16.3 mn units/year, up from 16.0 mn units/year in September. The daily selling rate was estimated at 49.8k units/day in October, down from 51.3k units/day in September. Although there was some variation across OEMs, the market overall appears to be building some momentum as we head into the holiday season. Recent changes in seasonality have made the annualized selling rate less reliable than has been the case in the past, but the rate registered its highest level for 2024 to date in October. According to initial estimates, retail sales totaled 1.15 mn units in the month, while fleet sales finished at 193k units, accounting for 14.3% of total volumes.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

While General Motors is accustomed to being the bestselling OEM, it had a particularly strong month in October, reaching 233k units. This positioned it well above second-placed Toyota Group, on 186k units. While Toyota Group was the only major automaker to see a YoY decline in volumes, it did have some positive news in the return of the Toyota Grand Highlander and Lexus TX, following the recent stop sales orders, although volumes were modest in October. Ford Group was once again the third largest OEM by sales, on 167k units. At a brand level, Toyota ranked first, but only by a narrow margin, with 159k units compared to almost 158k units for Ford. Chevrolet was also not far behind, on 149k units.

For the first time since June, the Toyota RAV4 returned to the top of the sales rankings with volumes of 39.4k units, beating the Ford F-150 which recorded 38.7k units. The RAV4 has recently been impeded by a lack of inventory, but this appeared to be less of an issue in October.

With the success of the Toyota RAV4, it was perhaps not surprising that the Compact Non-Premium SUV segment enjoyed its best market share since March 2024, at 21.1%. On the other hand, Midsize Non-Premium SUVs had a somewhat underwhelming month, recording a market share of 14.2%, which was virtually identical to that of the Large Pickup segment. Large Pickups have not outsold Midsize Non-Premium SUVs since July 2020, but the edge that the latter held over the former in October was just 206 units.

David Oakley, Manager, Americas Sales Forecasts, GlobalData, said: “Sales have generally disappointed for much of 2024, but October provided a pleasant change of pace. While the fundamentals of the market have probably not shifted to a great extent, some consumers appear to have been enticed by the gradual uptick in incentives, allied with greater vehicle availability and an easing in interest rates. A number of brands highlighted how Electric and Hybrid Vehicles performed better than gasoline-powered models in October, but to some extent, electrified vehicles are being boosted by higher incentives than their Internal Combustion Engine counterparts. Low levels of lease returns continue to be a headwind for the industry, but other purchase methods appear to be compensating for now”.

US inventory levels at the end of October rose by 4.3% to 2.9 mn units. With production levels outpacing demand, the days’ supply exceeded the 60-day threshold for the first time since June 2020. Further reductions in the fourth quarter are anticipated, with North American production now projected to decrease by 1% in 2024, equivalent to a loss of 150k units. There are lingering concerns as fleet sales have fallen short of projections, historically serving as a means to reduce high levels of inventory.

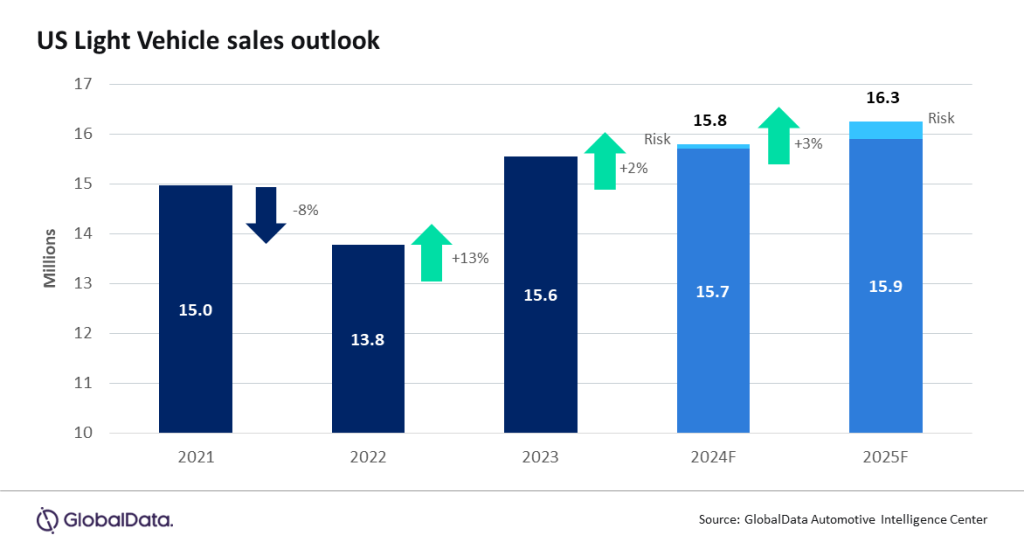

With just two months remaining in 2024, US sales are projected to reach 15.8 mn units/year, a slight decline from the previous month’s forecast of 15.9 mn units/year, even with the outperformance in October. Sales volumes for the year are anticipated to increase by 1.5% compared to 2023. However, if fleet sales continue at the last three months’ average of 190k units, LV sales will fall to 15.7 mn units/year. The forecast for 2025 has also been revised, with US sales now expected to reach 16.3 mn units/year, reflecting a 3% increase from 2024.

Jeff Schuster, Vice President Research and Analysis, Automotive, said: “After several tumultuous years, auto demand seems to have stabilized at current prices. We expect further price moderation in 2025 and additional interest rate cuts from the Federal Reserve to stimulate demand. However, 300k-500k units are at risk in our medium-term forecast, which projects the US market to reach 17.0 mn units by 2028, if prices continue to prohibit additional buyers from re-entering the market or if the fleet share of total LV sales does not return to the 18-20% range”.

Global outlook: September’s global LV selling rate came in at 89 mn units/year, slightly lower than August but consistent with the past five months. September experienced a 4.2% YoY decrease, marking the fourth consecutive month of decline compared to the same period in 2023. Year-to-date volume is now only 0.3% higher than in 2023, putting annual growth at risk as we progress through the fourth quarter. Similar to last month, Argentina, Brazil, and Russia were the only markets showing positive growth in September. As global LV sales appear to be leveling off, some of the previously expected acceleration in the fourth quarter has been tempered. The 2024 forecast now stands at 88.1 mn units/year, down 500k units from last month and with volume growth now projected at 1.4% for the year.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.