While inventory figures are not publicly available in Europe, recent events have highlighted that stock movements are a critical component when it comes to understanding the likely evolution of production volumes.

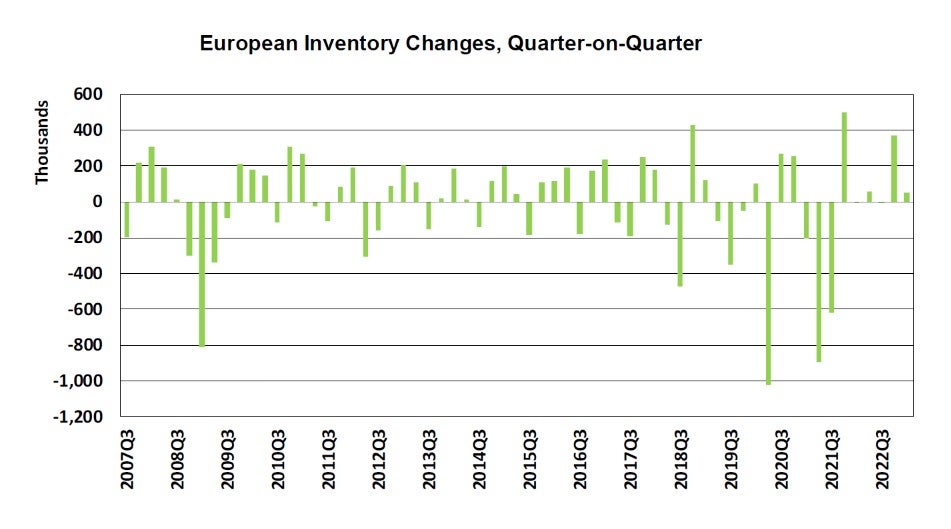

Following the Lehman Brothers collapse in 2008, OEMs were immediately faced with crashing market volumes. They responded by slashing output to minimise unplanned or unrequired stocks. But the scale of the crisis was such that this response proved to be too slow, leaving European OEMs sitting on circa one million Light Vehicles by the close of 2008, all of which were stuck in the supply chain and surplus to requirements.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

Of course, such shocks are not uncommon. Following the German reunification boom in 1990, the European market crashed in 1993.

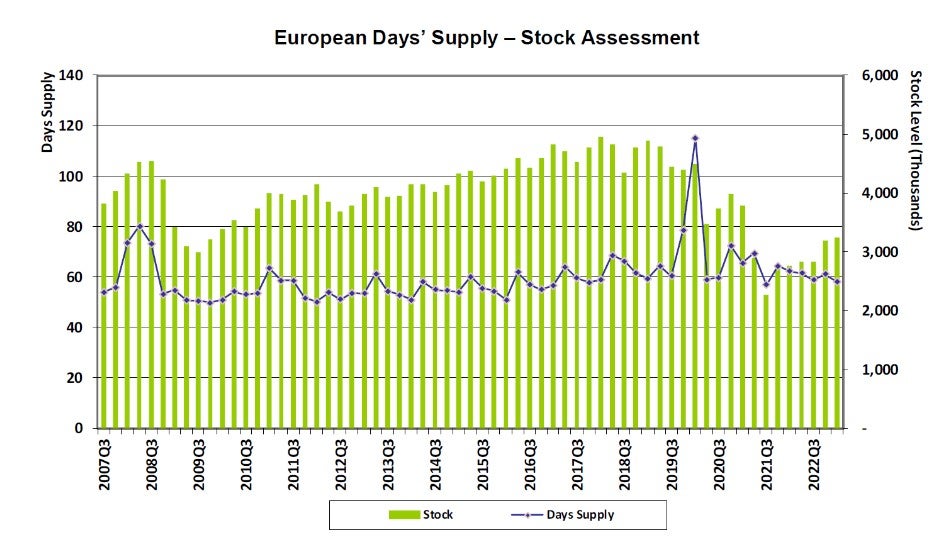

More recently, with the outbreak of the COVID-19 pandemic and the ensuing lockdowns, European OEMs saw days’ supply rocket to over 115 days in the first quarter of 2020. An ideal level for European days’ supply is around 60 days, meaning that the region was overstocked by 55 days!

Currently, European Days’ Supply is tracking at 60 days, our benchmark level of where the sector would like to reside.

But let’s not kid ourselves. European OEMs have been forced to trim build significantly, while incoming orders have slowed as both have been impacted by the chip shortage. Oddly enough, European Days’ Supply appears to be within the normal range because we are in an unusual position where both the flow of build and the flow of orders are being impacted at the same time and consequently, we have what might be considered a unique set of circumstances. Indeed, if the flow of orders had been in line with broader macroeconomic drivers, then the ‘real’ Days’ Supply situation in Europe was probably circa 40 days’ supply, rather than the 60 days which we report.

But there is some good news – European inventories have essentially been flat since the start of the year, and this contrasts with destocking of -1.7m cars suffered during the first three quarters of last year (itself worse than that suffered under the Lehman Brothers episode). We are looking for a recovery in Q4 but at +370k this would still be far from an exceptional performance.

So, unlike the Lehman Brothers-induced recession of 2008/9, the sector is in a much healthier position to respond to the market if supply difficulties ease. Much, therefore, rests on how the war in Ukraine and COVID-19 restrictions in China unfold.

Arthur Maher, Director or Research, LMC Automotive (a GlobalData company)