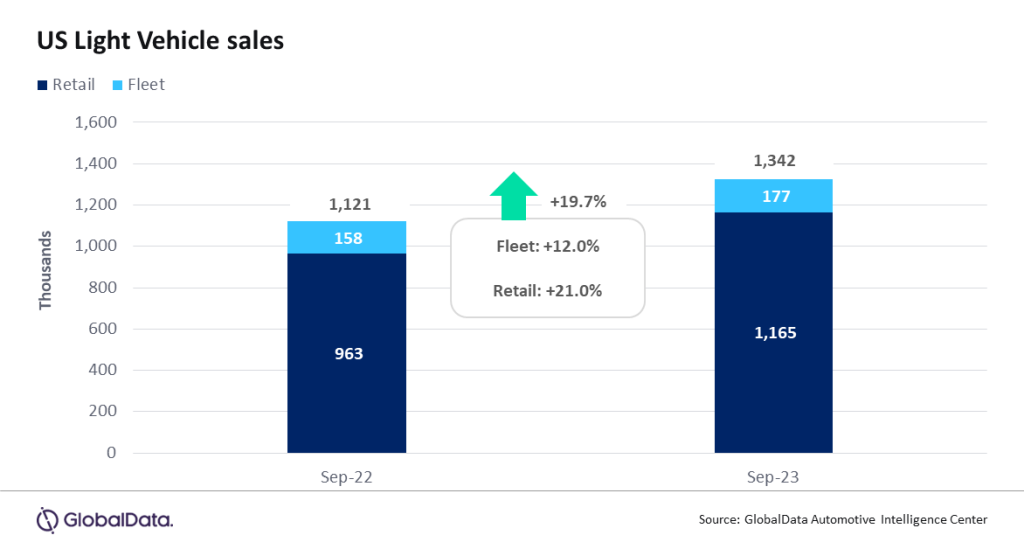

- According to preliminary estimates, Light Vehicle (LV) sales grew by 19.7% year-on-year (YoY) in September, to 1.34 million units. While the YoY gain is still flattered by weak sales a year ago, September delivered strong results despite the gloomy backdrop of UAW strikes that began mid-month. For now, inventory levels are still improving across the industry as a whole, and even though average transaction prices remain high, the supply of more affordable vehicles has increased.

- Global outlook – The global LV selling rate reached 99.7 million units in August and was at the highest monthly level since August 2018. The automotive market has consistently outperformed expectations throughout 2023 so far and is expected to remain around the 90 million unit selling rate again in September, leading to an increase in the forecast from 86.8 million units to 87.9 million units. The wildcards for the remainder of 2023 are set to be the US market—which may be influenced by the ongoing UAW strike—and China, with a price war that is attracting more consumers into the new-vehicle market but is negatively affecting OEM margins. The lift in the forecast for 2023 has also spilled into 2024, with the outlook being increased to 91.6 million units from 90.2 million units.

US LV sales totaled 1.34 million units in September, according to GlobalData. The annualized selling rate accelerated from 15.1 million units/year in August, to 15.7 million units/year in September, similar to the levels seen in June and July. The daily selling rate was estimated at 51,600 units/day in September, compared to 49,300 units/day in August. After a slightly disappointing August, September appears to have heralded a rebound in activity, with the Labor Day weekend possibly contributing to results that exceeded expectations. According to initial estimates, retail sales totaled around 1.165 million units, while fleet sales accounted for approximately 177k units, representing around 13.2% of total sales, the lowest share for 12 months.

David Oakley, Manager, Americas Sales Forecasts, GlobalData, said: “Recent headlines around the US auto industry have been focused on the UAW strike, but that impact will be delayed as the targeted OEMs continue to sell existing inventory. While one or two specific models are likely already seeing a negative effect on sales due to low days’ supply, on a wider scale the strikes may have spurred activity in September by nudging customers to make purchases before stocks run out. Still, sales were robust even among non-union OEMs, suggesting that longer-term trends around improved vehicle availability and a strong contribution from Premium brands – especially Tesla – also played a significant role”.

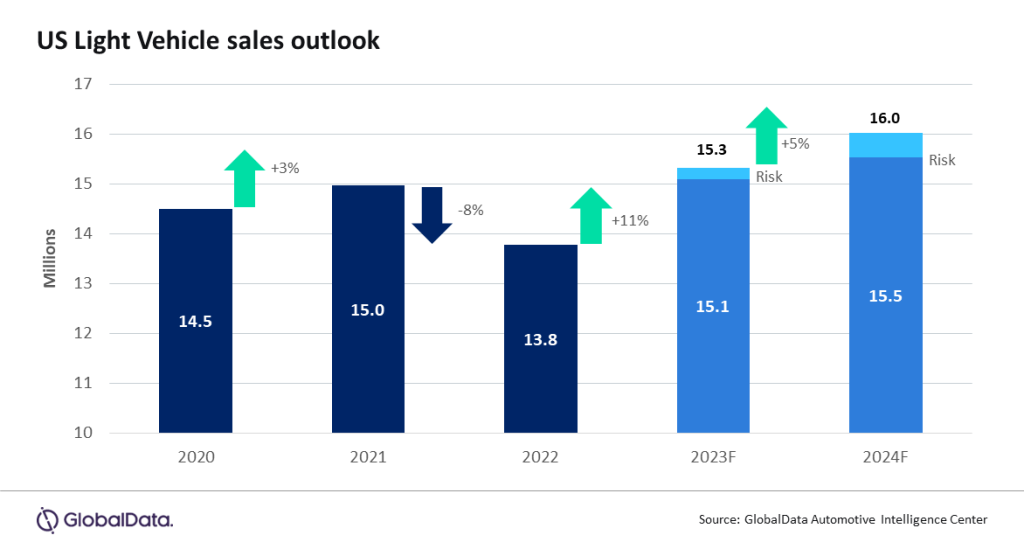

While there has been little impact to vehicle demand from the UAW strike, evident by September outperforming expectations, risks to the Detroit Three volume and topline increase as the strike continues. We are holding our forecast for 2023 at 15.3 million units, despite the strong performance, given the high level of uncertainty. While 2024 could benefit from volume lost in 2023, we are currently holding the forecast at 16.0 million units as well.

The ongoing duration of the strike and the expected increased severity are likely to cut into inventory and demand as early as October. However, levels are holding thus far, given the limited number of affected plants. For September, vehicle days’ supply is projected to hold in the 37–39 day range, which is just below where it was in August. Volume is expected to be at 1.9 million units as October starts.

At an OEM level, GM was once again the market leader with 225k units, claiming a market share of 16.8%. However, Toyota Group was the closest it has been to GM in terms of volume since October 2022, only around 21k units behind. At 15.2%, Toyota Group’s market share was its highest in 11 months. Ford Group was the third bestselling OEM in September, but with a modest market share by its standards, of 11.9%. For the first time ever, the Tesla Model Y is estimated to have led the market in September, with sales of 39.5k units, ahead of the Toyota RAV4 on 38.1k units. The Ford F-150, normally the market-leading model, dropped to third place with sales of just under 37k units, on the back of its lowest market share in 12 months. Looking at segments, Compact Non-Premium SUV set a new record high market share in September at 20.5%, beating the previous best that was set in July. Midsize Non-Premium SUV was second on 15.7%, followed by Large Pickup on 13.0%.

Jeff Schuster, Automotive Group Head and Executive Vice President, GlobalData, said: “As the market progresses in the 4th quarter, we find a growing number of risks and variables that could impact how sales end in 2023 and begin in 2024. The two sides remain far apart in the UAW contract negotiations and there is much at stake, as the outcome could have a profound effect on the makeup of the US auto industry in the future.”