Aston Martin reported another quarterly loss for the three months ended 31 March 2026, as its debt burden increased and additional funding support was secured from Lawrence Stroll’s Yew Tree Consortium.

Revenue for the first quarter rose 16% year-on-year to £270.4m ($365.2m), driven largely by higher ‘specials’ volumes, including 102 Valhalla deliveries.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

Gross profit climbed 44% to £93.9m, with gross margin improving to 34.7% from 27.9% a year earlier.

Despite the stronger revenue and margin performance, the company recorded a Q1 operating loss of £8.9m, although this represented a big improvement compared with the prior year’s Q1 loss of £67.3m .

Loss before tax also narrowed, at £65.5m compared to £79.6m in Q1 2025.

Adjusted EBIT improved by 12% to a loss of £56.9m, while adjusted EBITDA turned positive at £23.2m, compared with a loss of £4.4m in the same period last year.

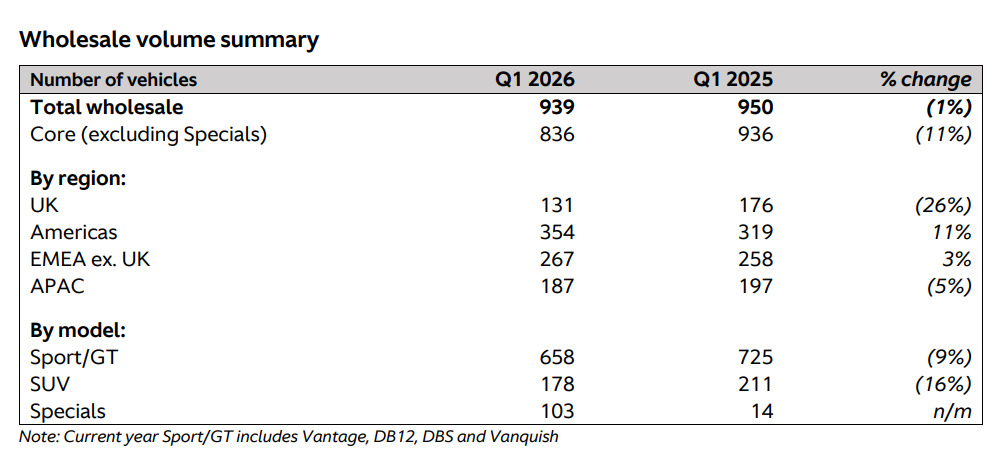

Wholesale volumes remained largely unchanged at 939 units, compared with 950 a year earlier, as lower core volumes were offset by higher Specials deliveries.

Regional performance was mixed, with UK volumes falling 26%, while the Americas rose 11%, EMEA (excluding the UK) increased 3%, and Asia-Pacific declined 5%.

Net debt increased to £1.46bn at the end of March 2026 from £1.38bn at the end of 2025, reflecting lower cash balances and higher gross debt.

Liquidity stood at £177.7m and rose to approximately £230m on a pro forma basis following the new £50m committed facility and proceeds from the sale of Formula One naming rights.

Aston Martin CEO Adrian Hallmark said: “Q1 2026 confirms that we are on track to deliver material financial improvement this year.

“In line with our full year guidance, Q1 2026 total wholesale volumes were similar to the prior year, while gross margin increased into the mid-30s driven by Valhalla deliveries and the benefits of our transformation programme.”

The company kept its full-year 2026 outlook unchanged, expecting wholesale volumes to remain broadly stable and financial performance to improve.

This is expected to be driven by a stronger product mix, including about 500 Valhalla deliveries, as well as operational efficiencies and a more balanced production schedule starting in the second quarter.

Aston Martin also pointed to ongoing uncertainty from macroeconomic and geopolitical conditions, including potential US tariffs, changes to China’s ultra-luxury car taxes, and supply chain dependencies affecting visibility.

The group said it will focus on cost optimisation, cash generation and liquidity management, while continuing its transformation programme and updated product cycle plan.

It expects to move towards breakeven adjusted EBIT margins in 2026 and improve free cash flow over the remainder of the year, with most outflows already incurred in the first quarter.