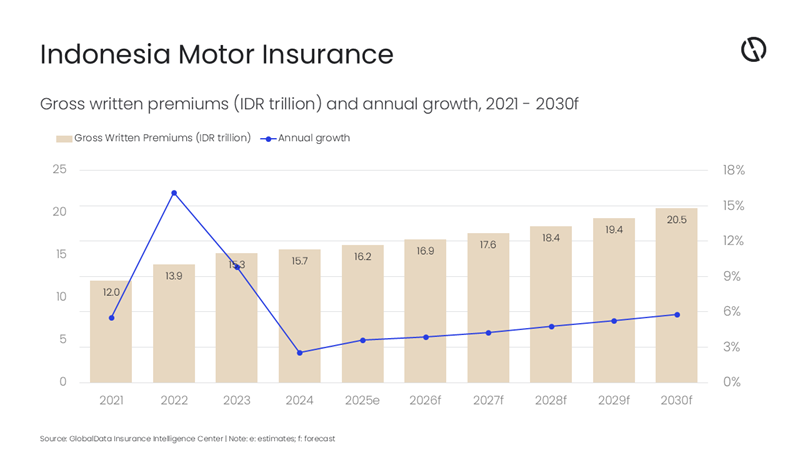

Indonesia’s motor insurance market is forecast to register a compound annual growth rate (CAGR) of 5%, with gross written premiums (GWP) increasing from IDR16.9 trillion ($1 billion) in 2026 to IDR20.5 trillion ($1.3 billion) in 2030, according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database estimates that the Indonesian motor insurance market will record an annual growth of 3.9% in 2026, supported by gains in digital distribution, product innovation, and strengthening underwriting discipline. The market is expected to face challenges such as rising vehicle prices, weakened purchasing power, and increased losses due to weather events. Despite these, the outlook remains positive as insurers embrace technology, develop electric vehicle (EV) insurance products, and improve risk assessment.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

Katam Prasanth, Senior Insurance Analyst at GlobalData, comments: “Indonesia’s motor insurance industry is being reshaped by EV purchase incentives (VAT and luxury tax exemptions), the emergence of EVs as a high-premium segment with distinct underwriting needs, and accelerating digitalization alongside favorable regulatory developments.”

According to the Association of Indonesian Automotive Industries, EV sales reached 55,255 units from January–September 2025, up 27.9% from 43,188 units over the same period in 2024. As EVs and hybrids expand within vehicle fleets, insurers are addressing new risk categories such as battery-related exposures, charging ecosystem considerations, and higher-cost specialized parts and repairs. These dynamics are encouraging product differentiation, including assessments of usage-based approaches and battery warranty-backed features.

Insurers are demonstrating innovation in EV insurance and distribution models, where customers can choose between comprehensive and total loss only (TLO) plans. Comprehensive plans include battery and charger cover, roadside and medical support, and extensive third‑party and personal accident protection, with added catastrophe and unrest coverage.

Under the Development and Strengthening of the Financial Sector (UU P2SK) law of 2023, the government can mandate motor third-party liability coverage. This was expected to take effect in 2025, but has been delayed, as the government has yet to approve the supporting legislation. Upon implementation, this is expected to significantly increase insurance penetration by covering currently uninsured vehicles, subject to the scope and enforcement set out in forthcoming government regulations.

Prasanth adds: “The industry is also managing premium softness, claims-cost inflation, and implementation uncertainty, making pricing discipline, operational efficiency, and stronger claims management increasingly critical.”

In 2025, motor insurance paid claims recorded an annual growth of 9.2%, due to higher mobility and an increase in minor accident frequency, alongside escalating exposure to weather-related events and other hazard-driven losses. These dynamics have increased focus on underwriting discipline, pricing adequacy, and claims management capabilities—particularly for catastrophe-linked events where protection levels remain uneven. Reflecting these initiatives, insurance claims are estimated to moderate in 2026 and record an annual growth of 7.4%.

Prasanth continues: “Insurers and insurtech partners are scaling digital journeys to reduce friction in buying and servicing policies. New AI-enabled platforms are being launched to support instant motor underwriting and policy issuance through digital risk assessment. These tools can widen access for underserved and underinsured segments by reducing documentation burdens, shortening quotation-to-bind timelines, and improving servicing responsiveness across policy lifecycle events.”

Furthermore, embedded insurance, insurtech partnerships, and more efficient policy/claims processing are becoming increasingly important—particularly in an environment of price sensitivity.

Prasanth concludes: “The Indonesian motor insurance market is expected to remain on a growth path through 2030. To capture this opportunity, insurers will need to translate digital and AI spend into real adoption, improve protection in underinsured segments, and ensure underwriting and capital management keep pace with a more complex risk environment.”